Distinguished Members of the Press,

Esteemed Guests,

Welcome to our press conference, where we will be sharing the 2024 results of the “ISO – Türkiye’s Top 500 Industrial Enterprises Survey,” now in its 57th year.

Our Deputy Chairmen İrfan Özhamaratlı and Cemal Keleş and I welcome and greet you on behalf of the Istanbul Chamber of Industry.

Before we begin, let me take a moment to wish you a joyful and meaningful Eid al-Adha, a time when hearts come together and bonds are strengthened. I hope you spend the holiday in peace and happiness, surrounded by your loved ones.

The ISO 500 study was first launched in 1968, originally covering just 100 companies. By 1978, that number had grown to 300, and since 1981, we have been publishing it as “Türkiye’s Top 500 Industrial Enterprises.” I imagine many of you are also curious about our earlier editions. In response to that interest, for the past seven years, we have been publishing a historical version alongside the latest ISO 500 report –sharing the study from exactly 50 years ago. This year is no exception. In your folders, you will find a facsimile of the report we released in 1975. Alongside the latest data, I think you will find the 1975 edition offers some fascinating insights into the state of our economy and industrial sector in the 1970s.

I would like to take this opportunity to pay tribute to those who first launched this report, an important archive of Türkiye’s economic and corporate history, and to everyone who has carried it forward with care and professionalism over the decades.

This is a project that takes real dedication every year. I would especially like to thank our Economic Research and Corporate Finance Department, along with our consultants, who work with great care and discipline, almost like entering a months-long retreat, to analyze the data we receive from industrial companies and produce the ISO 500 Survey. Of course, the true protagonists of this research, which can be seen as a kind of “health check” for our industry, are the industrialists themselves and their companies. We sincerely thank these valued stakeholders who shared their critical data with us.

Distinguished Members of the Press,

Before we dive into the much-anticipated results of our study, I would like to revisit a few key economic developments in Türkiye and the world to help contextualize the findings.

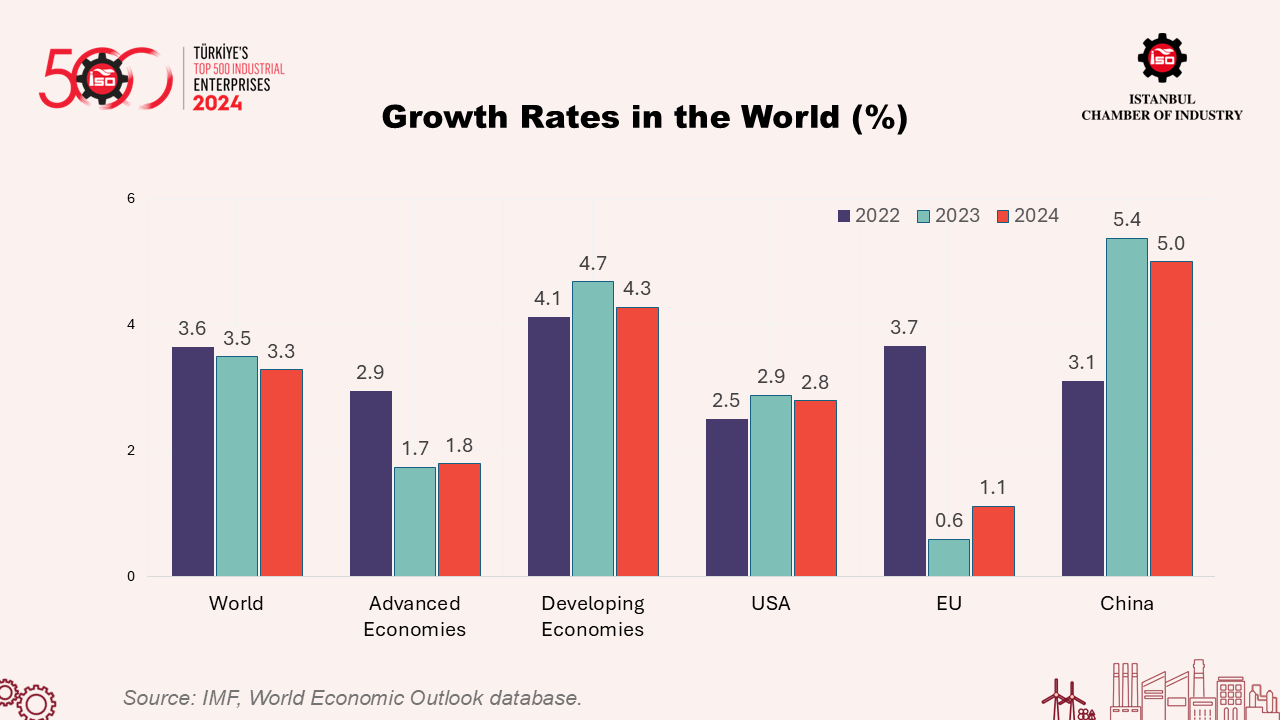

The year 2024 saw a deepening of global economic and trade fragmentation, alongside continued geopolitical uncertainty. In particular, the prolonged tight monetary policy stance in the United States and the dollar appreciation put further pressure on emerging markets. Amid heightened sensitivity to financial conditions and global trade risks, manufacturing sectors globally underperformed compared to services.

Among major economies, the only country that managed to stand out in 2024 was the United States, with a growth rate of 2.8%. Our main export market, the European Union grew by only 1.1%. China, which has dominated the global economy in recent years, delivered a performance far below the nearly 9% average annual growth it achieved between 2000 and 2019. Indeed, growth in China slowed from 5.4% in 2023 to 5.0% in 2024.

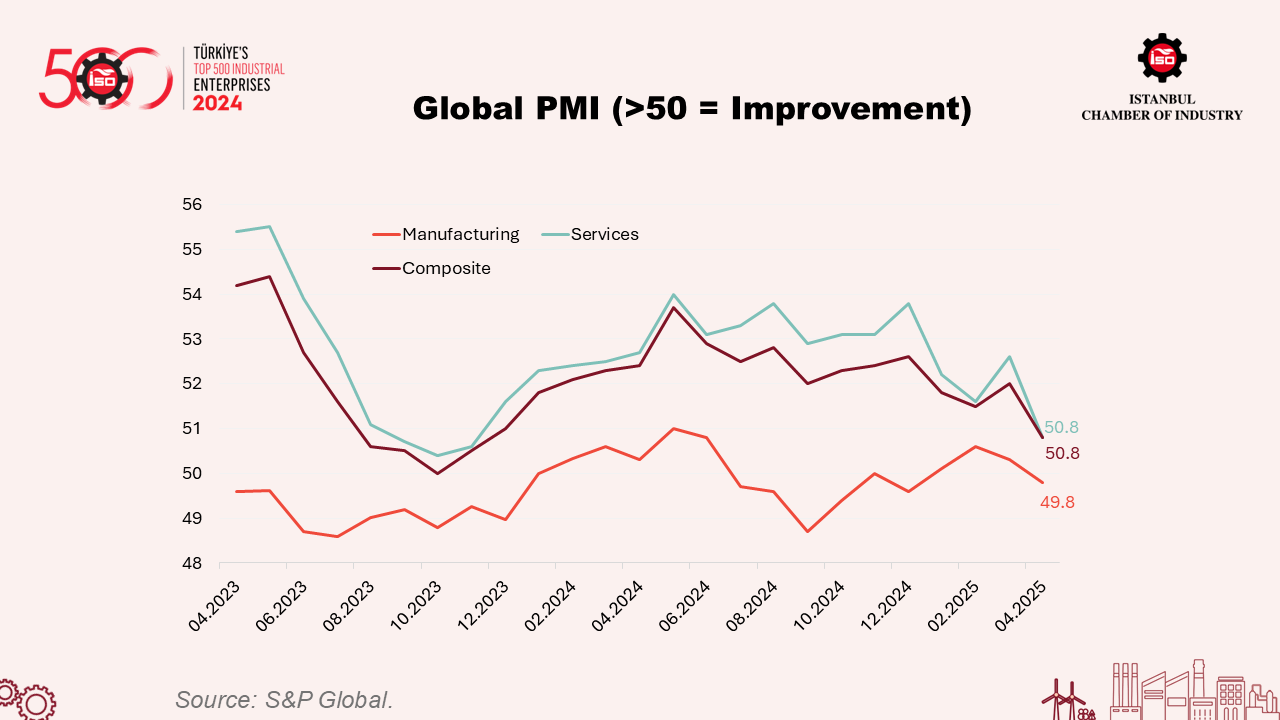

Global Manufacturing PMI data also confirm the sluggish outlook I just highlighted in the global economy. The Global Manufacturing PMI hit a historical low of 48.7 in September 2024 and remained stagnant throughout the year. To this stagnation, we must now add a new layer of uncertainty –additional fragility in the global trade system tied to the onset of a second Trump administration.

From Türkiye’s perspective, one of the strongest global headwinds last year was undoubtedly the weak growth in our main export markets, particularly the EU. On the upside, the normalization trend in commodity prices emerged as a supportive factor for our economy. However, the weak global outlook, on the one hand, and the tightening of monetary policy – especially from the second quarter of 2024 onward as part of the domestic disinflation program – on the other, placed serious pressure on our industry.

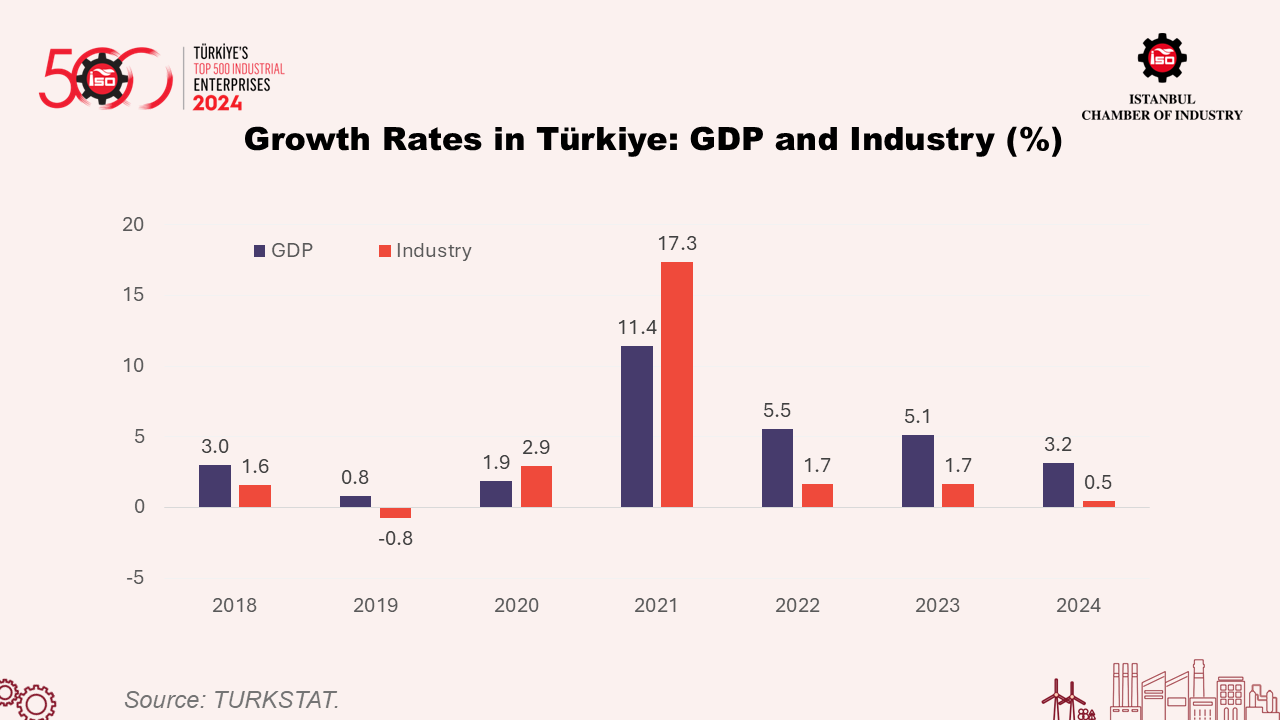

Under tight monetary policy, credit supply contracted significantly, and as expected, investment appetite weakened. This impact is clearly reflected in Türkiye’s and the industrial sector’s growth figures. Following GDP growth of 5-5.5% in 2022-2023, our growth rate slowed to 3.2% in 2024. As in the past three years, growth in the industrial sector lagged behind the overall economy and remained at just 0.5%.

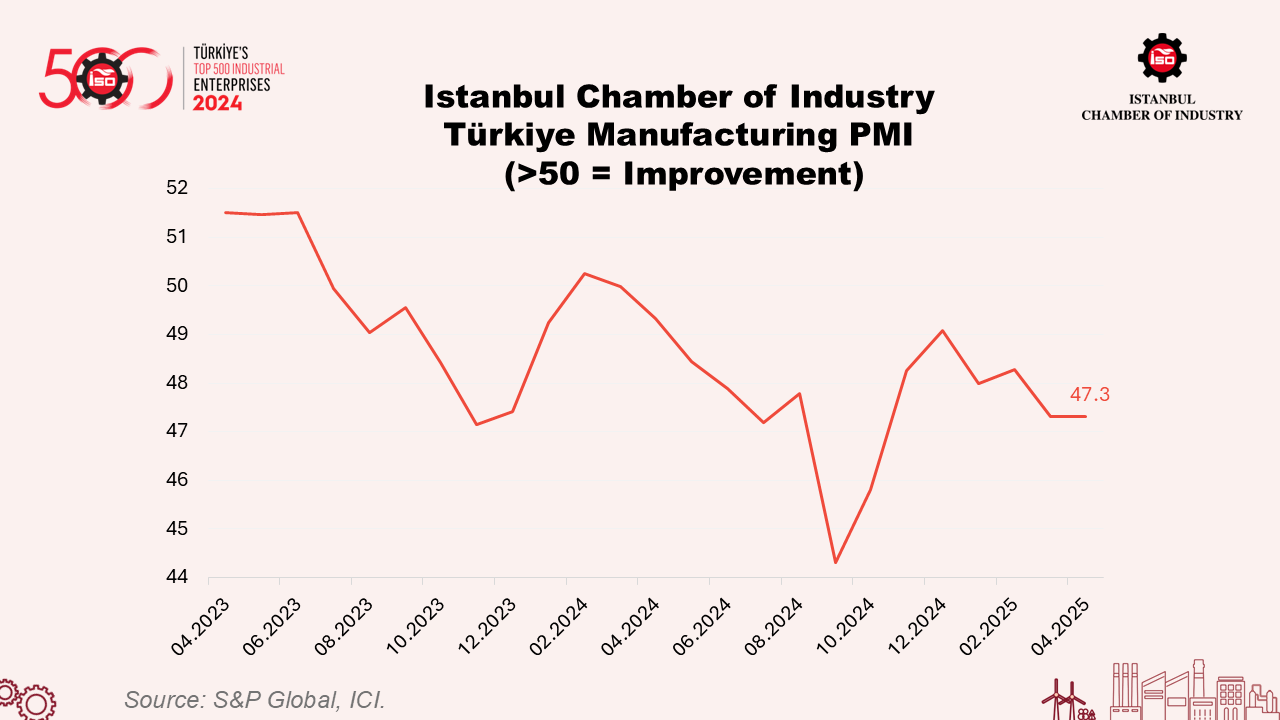

We also observed this loss of momentum clearly in the ISO Türkiye Manufacturing PMI data throughout the year, with global economic slowdown and tight domestic monetary policy standing out as key drivers. Except for a mild uptick in February 2024, the ISO Türkiye Manufacturing PMI has remained below the critical 50 threshold for nearly two years.

Esteemed Members of the Press,

Dear Guests,

The results of the ISO 500 - Türkiye’s Top 500 Industrial Enterprises study offer valuable insight into how recent global developments and the domestic disinflation program have shaped the performance of the industrial sector.

In just a moment, we will look at these impacts in concrete, numerical terms. But before we delve into the data, I would like to briefly reflect on the broader picture these results reveal, particularly the heavy burden borne by our industrial sector during this economic conjuncture.

When we look at the 2024 ISO 500 results, we are faced with historically negative outcomes across three key indicators. First, as we will soon see, ISO 500's production-based net sales have declined in real terms for three consecutive years.

Second, the long-standing issue we have raised in each year’s ISO 500 meeting – the fact that a substantial share of industrial profits is consumed by financing costs – has reached a critical point. The familiar line “industrialists are spending half their earnings on financing” no longer captures the gravity of the situation. For the first time in recent years, many industrialists have had to allocate almost all of their profits to cover financing expenses.

Third, I want to highlight two more figures that show just how far profitability ratios have fallen below their 10-year averages. ISO 500’s operating profit margin, which averaged 10.4% between 2014 and 2023, dropped to 6.2% in 2024. Likewise, Return on Sales (ROS), which averaged 7.1% over the past decade, declined sharply to 2.6% last year – another key indicator that deserves close attention.

Distinguished Members of the Press,

Esteemed Guests,

I will not overwhelm you with more figures. But even these few indicators paint a very clear picture of the severe operational pressures facing the industrial sector today. That is why I would like to say a few words about the factors that created these conditions, and the stance and sacrifices our industrialists have demonstrated in response, both historically and today.

As you may recall, nearly three years ago, when the first decisions were made to depart from rational economic policies, we warned that the outcome would be financial instability and high inflation.

And we now see that bringing inflation back under control comes at a very high cost. Unfortunately, it is the industrial sector that has borne the brunt of that cost.

This is precisely why we have consistently voiced our support for the Medium-Term Program (MTP). As industrialists, even though we did not create the problem, we have shown – and continue to show – the strongest belief, the greatest patience, and the most steadfast support for the program’s success.

Throughout this period, we have highlighted through many platforms and numerous metrics, including the ISO Türkiye Manufacturing PMI you saw earlier, just how difficult operating conditions have become for industry. But the clearest and most undeniable evidence of this is the ISO 500 report we are sharing with you today.

When we look at real growth, profitability, financial expenses, and other key metrics, it becomes clear that 2024 was one of the most challenging years in the history of the ISO 500. Despite making the greatest sacrifices during the MTP process, the industrial sector ended 2024 with almost no growth – a stark indicator of its current state.

Therefore, if the MTP is to succeed, we must also acknowledge that the heaviest burden of the program has fallen on the shoulders of industry.

As industrialists, we reaffirm today the trust and belief we have held in the MTP over the past two years. And as we have repeatedly stated, we continue to view the MTP’s targets, decisions, and implementation as essential references, particularly in safeguarding the “financial stability” we all recognize as critical. That said, as we look ahead, it must be a shared understanding that any perception of drifting away from the program’s core objectives must be firmly avoided.

Distinguished Members of the Press,

Esteemed Guests,

Following this brief overview, now let us proceed to the findings of our ISO Türkiye's Top 500 Industrial Enterprises-2024 survey.

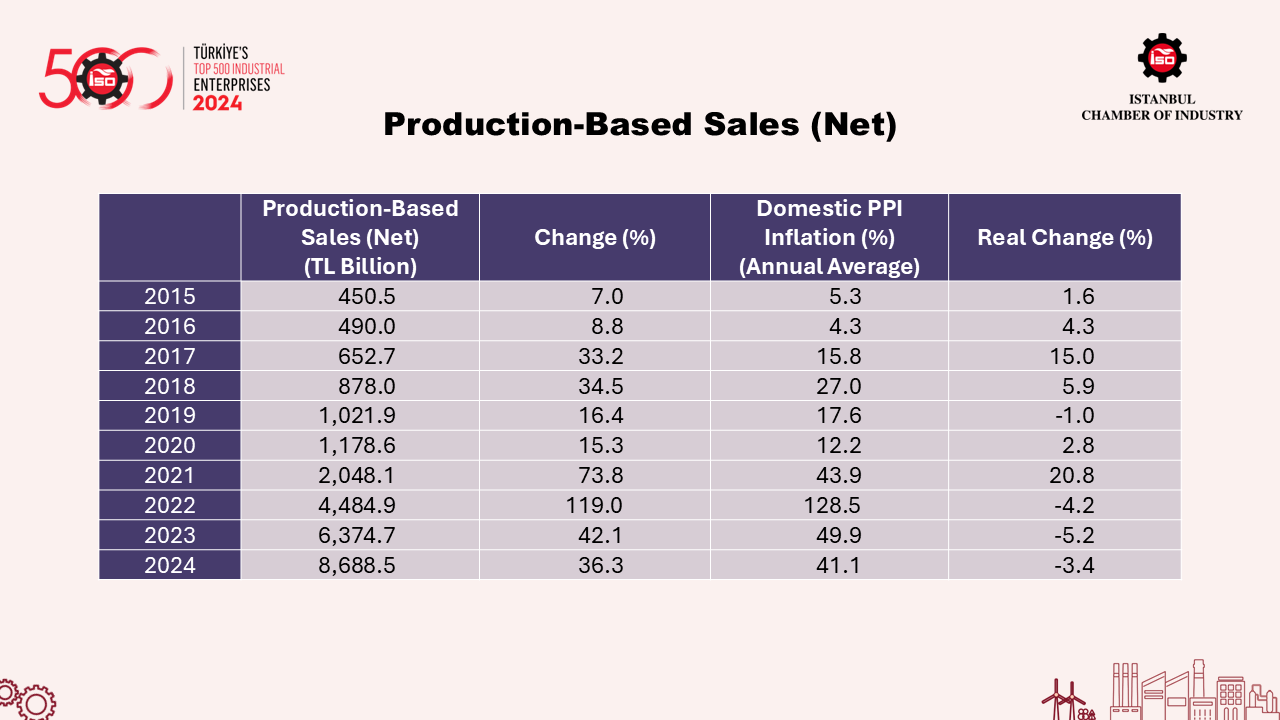

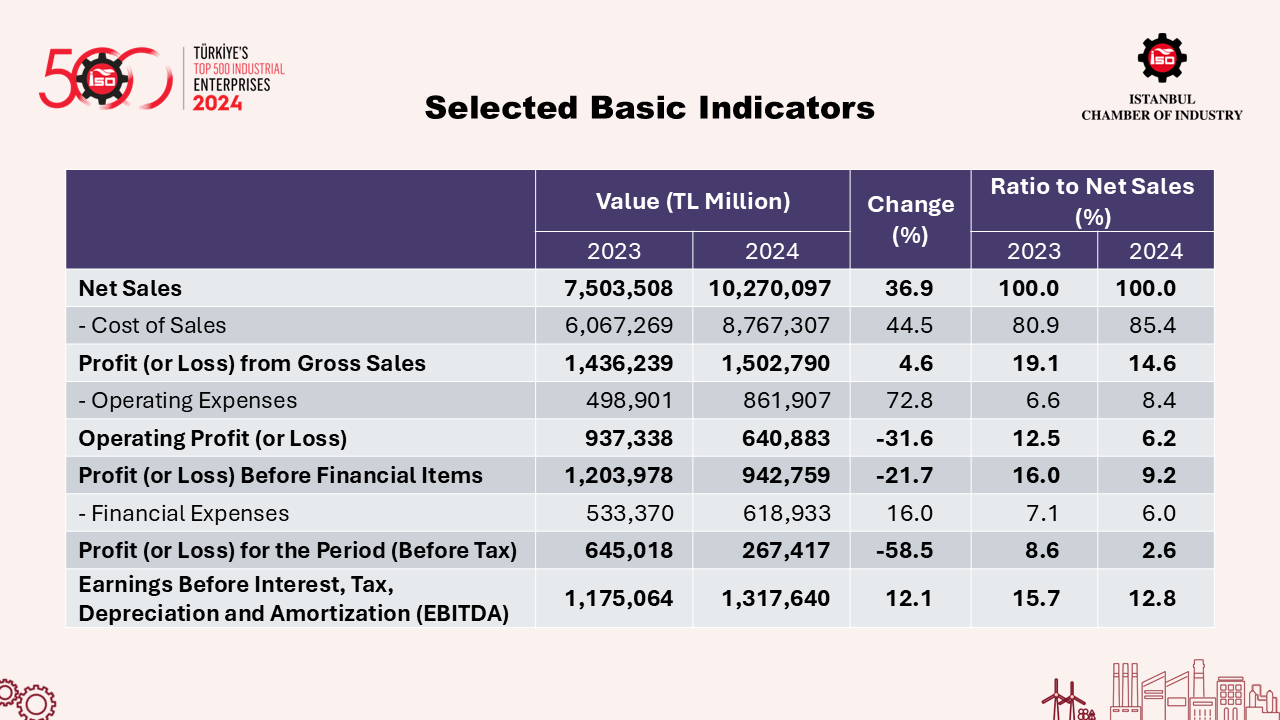

Our first table focuses on production-based sales. The most notable point here is that production-based sales among ISO 500 companies have declined in real terms for three consecutive years. While ISO 500 companies increased their production-based sales from TL 6.4 trillion to TL 8.7 trillion in 2024, an increase of 36.3%, this growth fell short of the previous three years. Compared with the growth figures in recent years, the weakening in production-based sales performance is clear.

When adjusted for the 2024 average annual Domestic Producer Price Index (D-PPI) of 41.1%, production-based sales fell by 3.4% in real terms. This marks the third year in a row of real contraction, following a 4.2% decline in 2022 and 5.2% in 2023 – once again underscoring the challenging environment facing our industrial sector.

There is no doubt that both domestic and global factors played a defining role in this weak performance in 2024. On the domestic front, monetary policy became increasingly tight. As a result, a gradual slowdown in domestic demand began to weigh on industrial sales.

Externally, subdued demand in key markets pressured export growth in 2024. Moreover, the sector’s international competitiveness was weakened by several factors: the inability to fully pass rising cost pressures onto sales prices, the real appreciation of the Turkish lira, and the adverse exchange rate impact resulting from a strong dollar These combined effects further dampened sales performance.

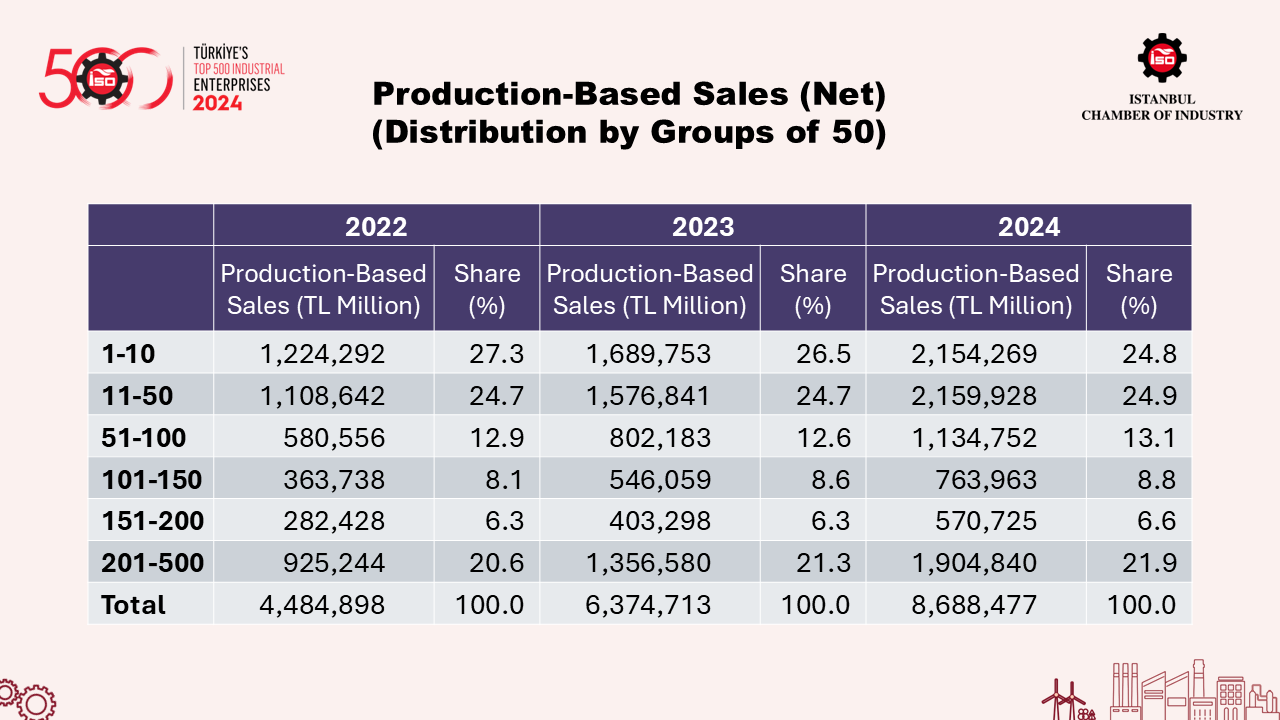

Looking at the distribution of production-based sales by groups of 50, we see that the top 10 companies account for nearly 25% of total ISO 500 sales. The top 50 companies, whose share has hovered around 50% for many years, maintained that share again in 2024. This clearly reflects the significance of economies of scale.

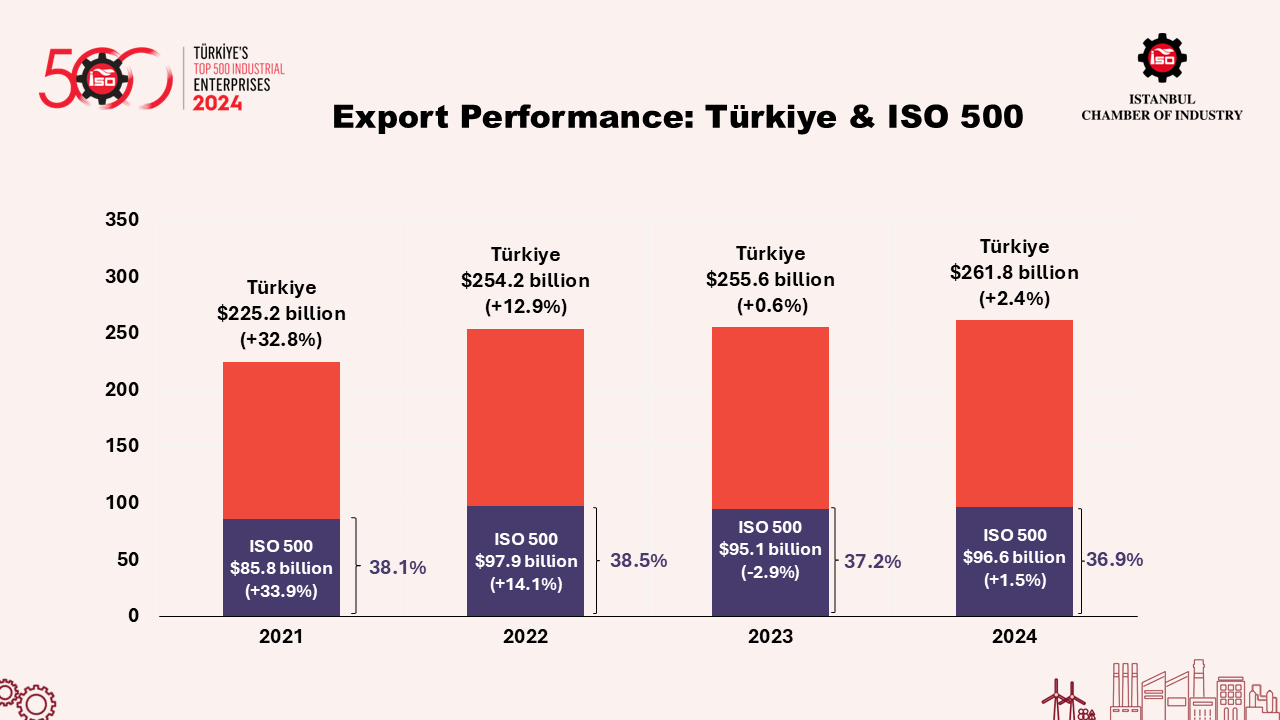

Turning to ISO 500’s export performance, we see that its share within Türkiye’s total exports remained stable. Türkiye’s total exports increased by 2.4% in 2024, reaching USD 261.8 billion.

In the same year, ISO 500 exports rose by 1.5%, from USD 95.1 billion to USD 96.6 billion. ISO 500’s export growth in 2024 lagged behind Türkiye’s overall export growth by 0.9 percentage points, suggesting that tougher global competition had a disproportionate impact on these companies.

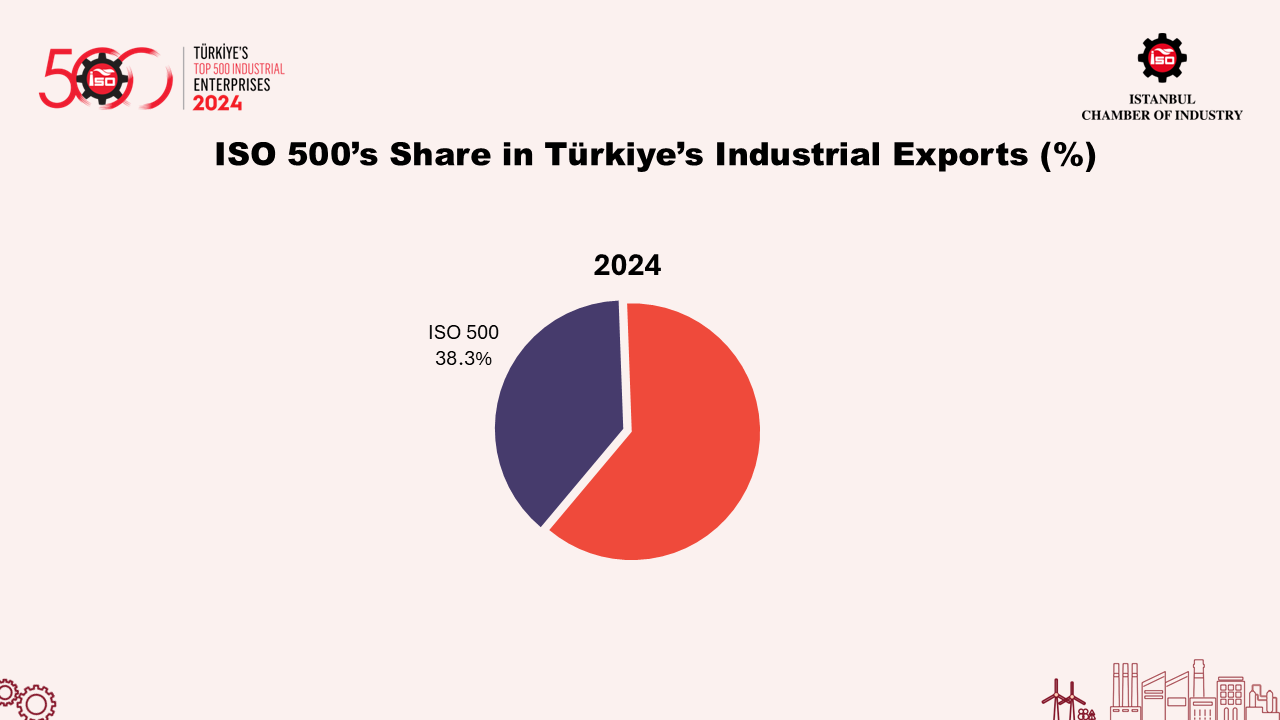

When we look at ISO 500’s share within industrial exports, it is clear that the group continues to represent a significant portion of the country’s export performance. In 2024, ISO 500 accounted for 38.3% of Türkiye’s industrial exports, maintaining a level close to the 40% threshold.

One of the most striking tables in this year’s report is right here. It shows just how sharply industrial sector profits declined in 2024. In addition to weak sales stemming from stagnant domestic and external demand, rising costs had a clear negative impact on operating profitability.

ISO 500’s total operating profit declined by 31.6% in 2024, falling from TL 937 billion to TL 641 billion. In line with this, the operating profit margin fell from 12.5% to 6.2%. As noted earlier, this margin is significantly below the 2014-2023 average of 10.4%.

Pre-tax profit and loss for the ISO 500 also dropped sharply by 58.5% from TL 645 billion to TL 267 billion. One of the most notable figures in this context is the dramatic fall in Return on Sales. ISO 500’s Return on Sales declined from 8.6% to 2.6%, well below the ten-year average of 7.1%.

The decline in pre-tax profit and loss was partially affected by a TL 65.2 billion net loss recorded as part of inflation accounting adjustments. However, the impact of this loss on Return on Sales was limited to just 0.6 percentage points. In other words, without the inflation adjustment, ISO 500’s Return on Sales would have been 3.2%, not 2.6%.

Lastly, when we look at another key profitability indicator, EBITDA (earnings before interest, taxes, depreciation, and amortization), we see only a modest 12.1% increase, from TL 1.2 trillion to TL 1.3 trillion. This limited growth caused the EBITDA margin to fall by 2.9 percentage points, from 15.7% to 12.8%. This ratio also fell below the 2014-2023 average of 13.7%, further confirming that the 2024 results were weaker across the board compared to previous years. As we can see, all profitability indicators for ISO 500 in 2024 point to a negative picture.

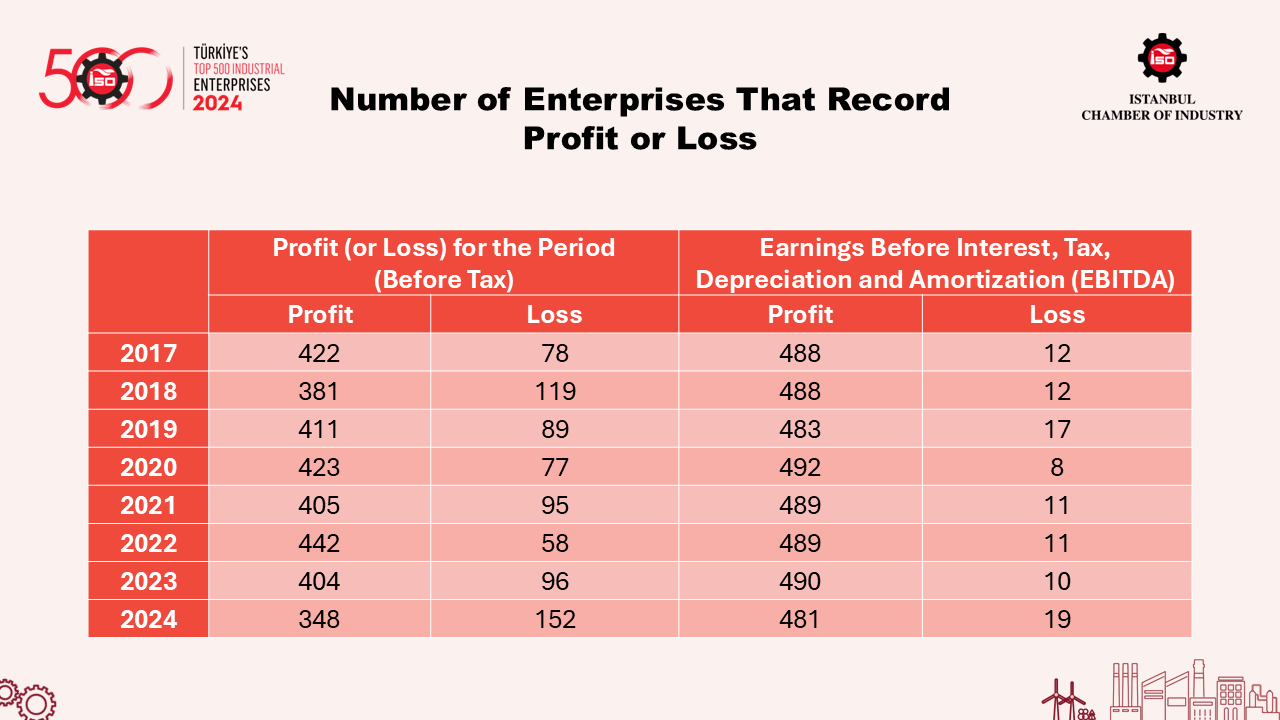

The number of companies reporting pre-tax losses rose significantly – from 96 to 152.

The number of firms posting losses on an EBITDA basis also increased, though more moderately, from 10 to 19.

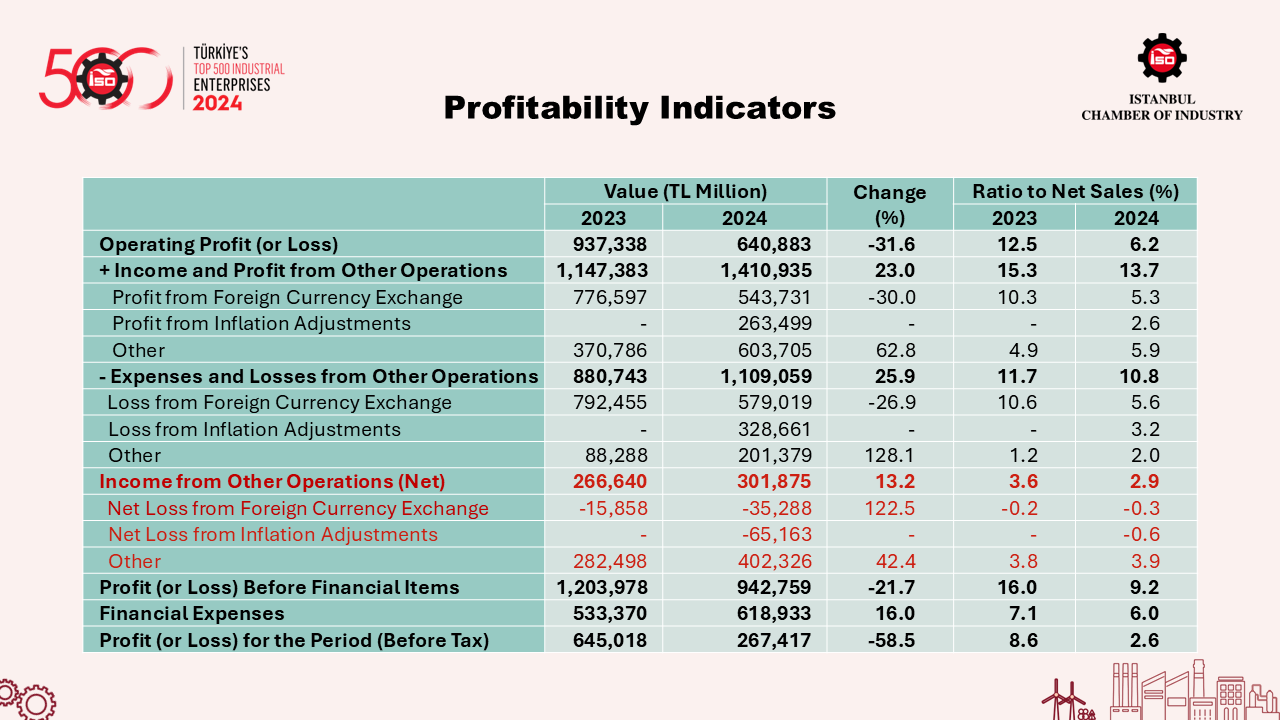

This table provides an overview of the profitability components within ISO 500. When we compare it with last year’s data, we again see a net foreign exchange loss reported in 2024. In the same year, inflation accounting also resulted in a net loss from adjustments.

Excluding foreign exchange and inflation adjustment effects, ISO 500 companies recorded TL 402 billion in net profit from other income in 2024. Still, this figure as a share of production-based sales edged up only slightly, from 3.8% to 3.9%, indicating limited impact.

I would like to kindly remind you that these revenues include items such as interest income, dividend income from affiliates and subsidiaries, gains and losses from securities, sales of fixed assets, commissions, and other similar items.

Distinguished Members of the Press,

Esteemed Guests,

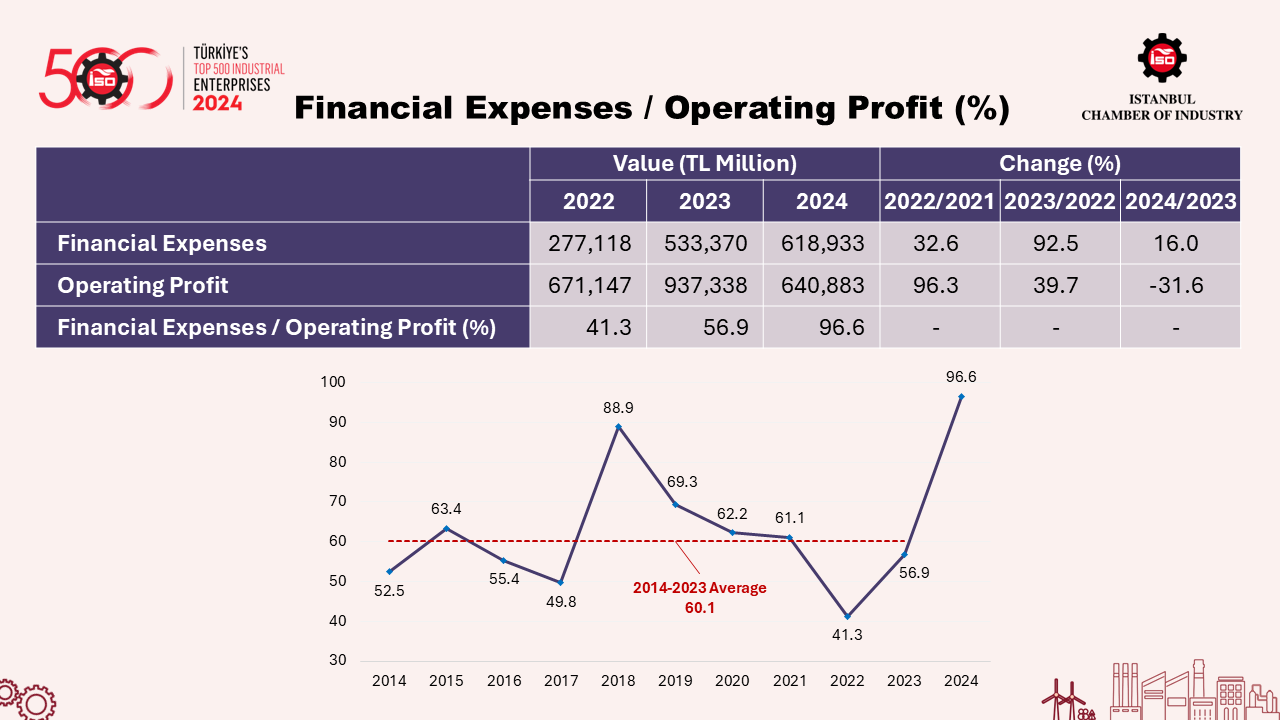

What you see here is a detailed breakdown of one of the most fundamental challenges facing industrial companies: financial expenses. The impact of financial expenses on ISO 500’s profitability remained significant in 2024.

As we look closer at the figures, we see that high interest rates on Turkish lira-denominated loans, combined with relatively flat exchange rates, drove many firms toward foreign currency loans, which offered more favorable terms in terms of cost and maturity. Meanwhile, high interest rates and weaker demand conditions dampened firms’ appetite for borrowing. Taken together, these dynamics suggest that ISO 500 companies managed their financial expenses more effectively in 2024.

However, despite relatively better cost management, most companies spent nearly all of their earnings on financial expenses, primarily due to notably weak operating profits.

To be specific: in 2024, ISO 500’s financial expenses rose by just 16% – well below inflation – reaching TL 619 billion. Meanwhile, due to weak sales and rising costs, operating profit dropped sharply by 31.6% to TL 641 billion.

As a result, the ratio of financial expenses to operating profit rose markedly, from 56.9% to 96.6%. This is significantly above the 2014-2023 average of 60.1%, and I believe it is important to emphasize that.

This long-standing issue has become a kind of chronic wound. And while it is important to point out the structural problems around access to finance and the quality of financing, I also believe we industrialists must take some responsibility ourselves. Because even if this year’s ratio was exaggerated by low operating profits, the fact that the 10-year average remains above 60% speaks for itself:

In my view, finance remains the most underestimated discipline in the industrial sector. We keep our distance from financial instruments widely used around the world. We do not make sufficient use of tools that could help us manage risk. Instead of waiting for external support or incentives, we need to take a hard look at ourselves and embrace the diverse instruments that the rest of the world is already using.

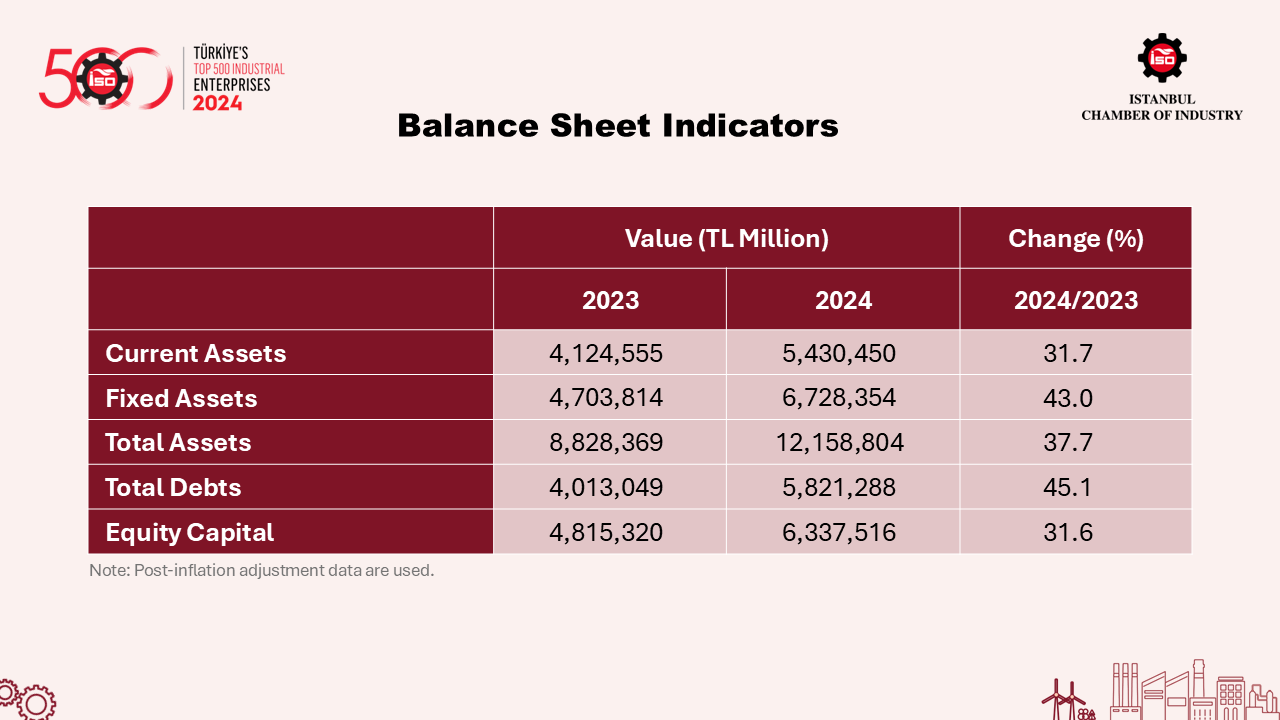

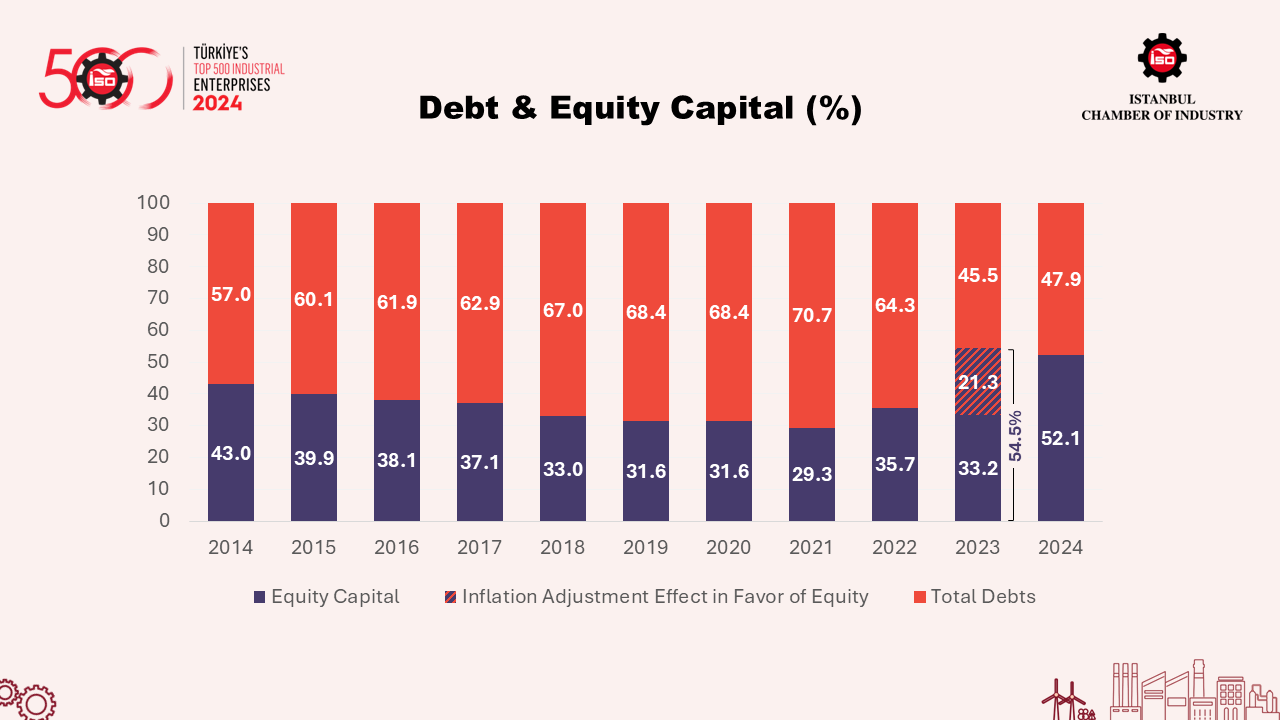

As you know, inflation accounting in 2023 led to significant increases in balance sheet indicators, especially on the asset and equity sides. When we examine ISO 500 companies for 2024, we see that the impact of inflation adjustments has been more moderate.

As shown in the table, current assets grew by 31.7%, while fixed assets increased by 43%. As a result, total assets rose by 37.7%.

On the liabilities side, equity capital rose by 31.6%, while total debt increased at a faster rate of 45.1%.

ISO 500 data also reveal noteworthy figures in terms of debt-to-equity capital ratios. As you may recall, last year’s inflation adjustment applied to non-monetary balance sheet items primarily affected capital structure via equity capital, playing a role in improving the distribution of financial resources.

In 2024, however, while equity capital increased by 31.6% compared to the previous year, total debt rose at a faster pace of 45.1%. As a result, the share of equity capital in total assets decreased from 54.5% to 52.1%, while the share of total debt rose from 45.5% to 47.9%. Nevertheless, the share of equity capital in total assets remained above 50%.

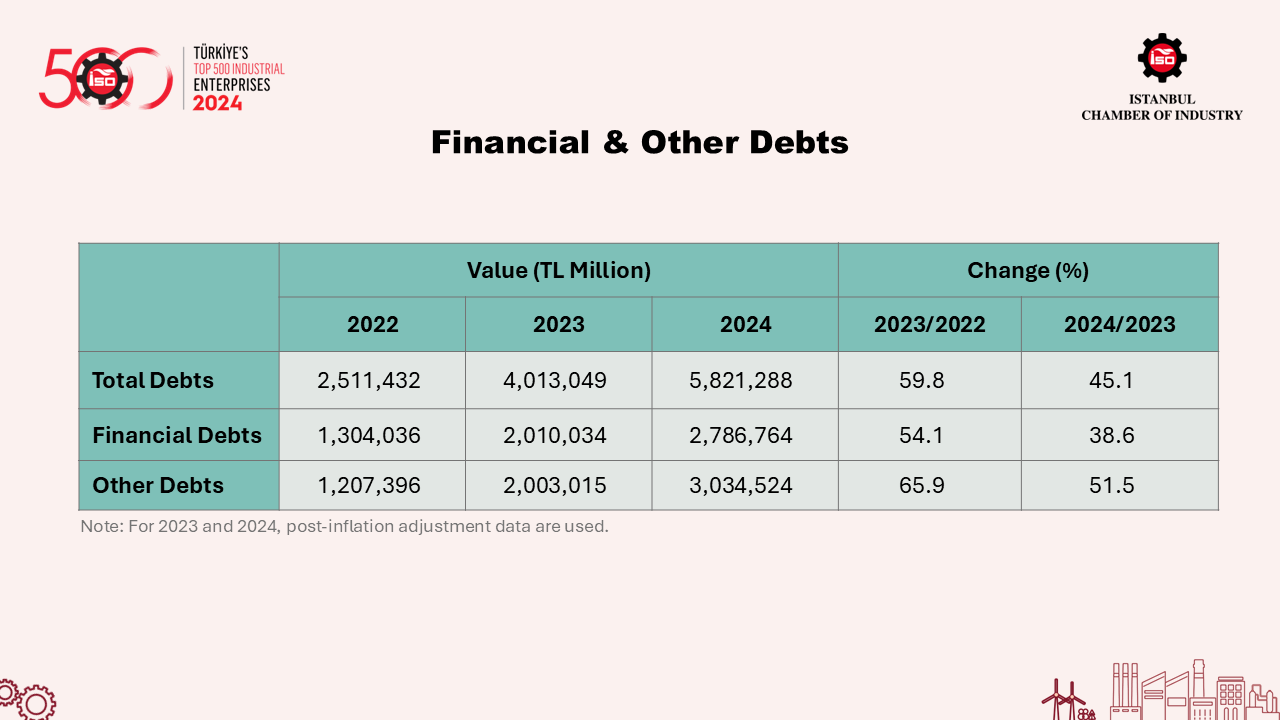

This table, which analyzes ISO 500 in terms of financial and other debts, shows that total debt, which had increased by 59.8% in 2023, grew by 45.1% in 2024.

A breakdown of subcategories reveals that the increase in financial debt was limited to 38.6% in 2024. Other debts, on the other hand, increased by 51.5%.

As in the previous three years, other debts in 2024 once again outpaced the growth of financial debt. As expected, higher interest rates and tightening access to credit slowed the growth of credit usage in the industrial sector. It is also evident that industrial enterprises met much of their net working capital needs primarily through other debts.

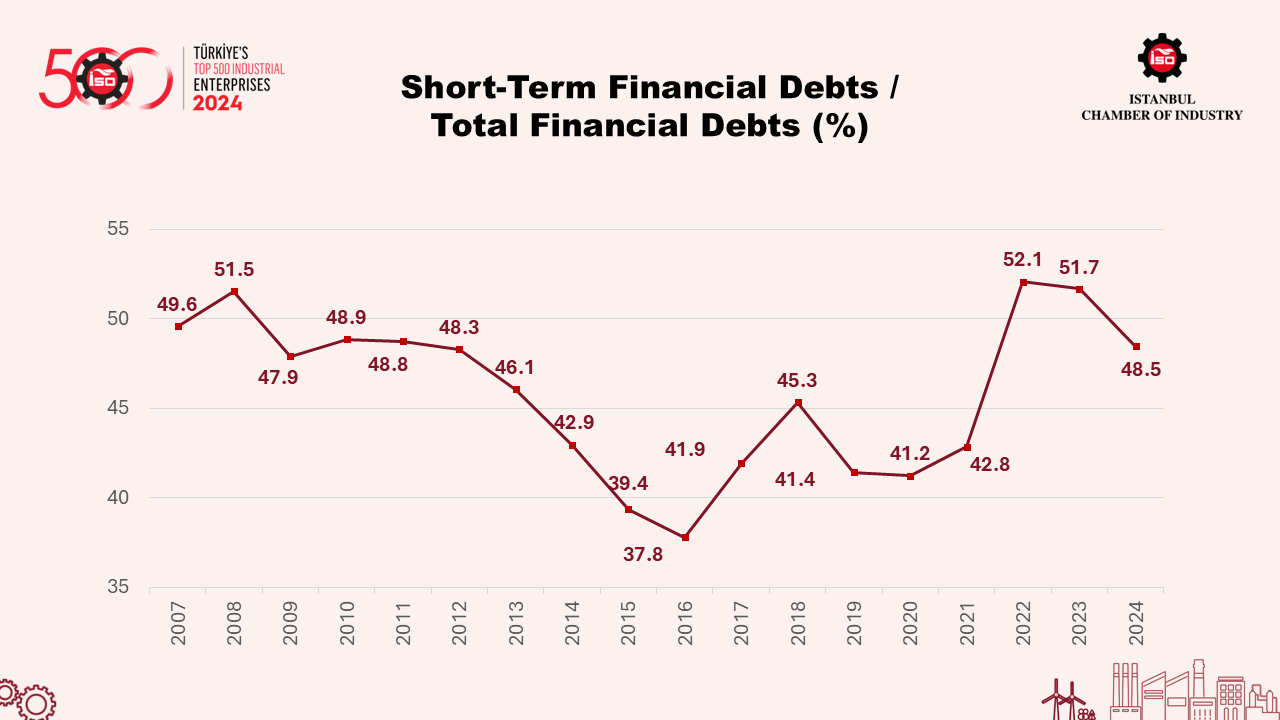

Here we see the share of short-term financial debt within ISO 500’s total financial debt. This share, which stood at 51.7% in 2023, fell by 3.2 points to 48.5% in 2024.

This change stems from the fact that while short-term financial debt increased by just 30%, long-term financial debt grew at a much faster rate of 47.9%.

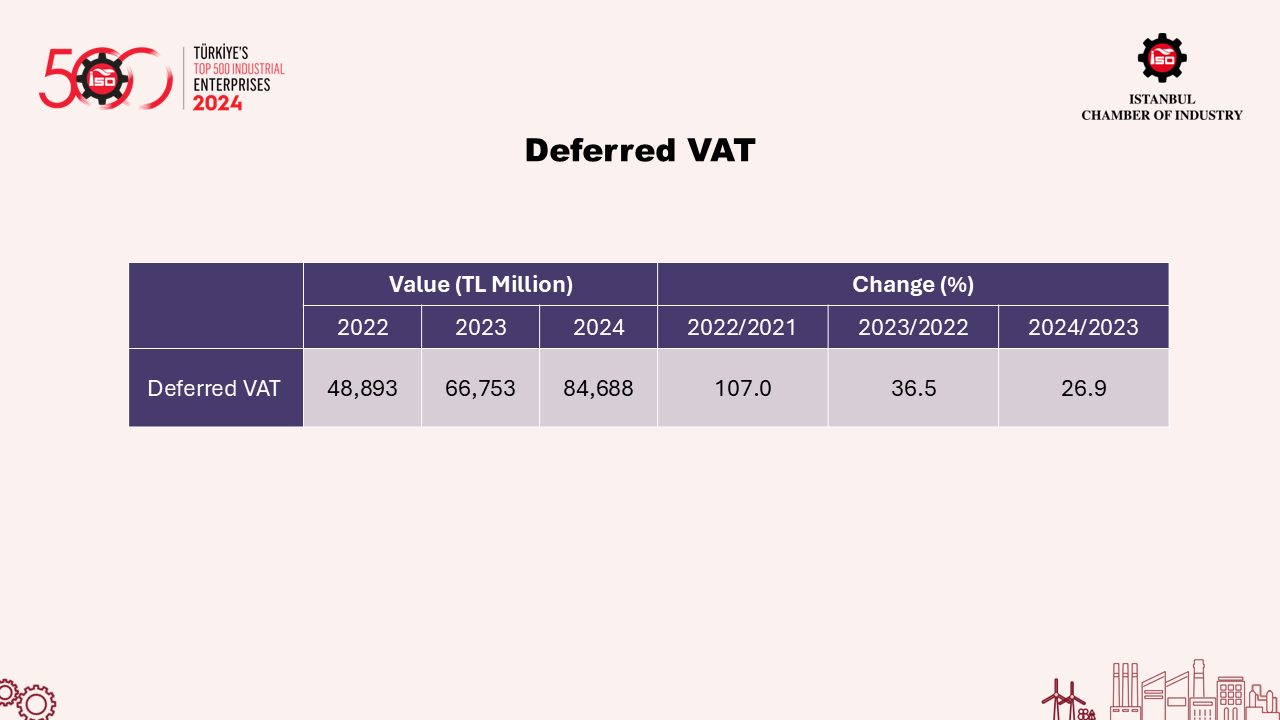

When we consider this picture, it becomes clear that the long-standing issue of outstanding VAT receivables – a topic we have raised for years and for which we have proposed solutions – still remains unresolved. The VAT burden accumulating on the ISO 500 increased by 26.9 percent to reach TL 85 billion.

Although this increase is somewhat more favorable than previous years by remaining below inflation, we continue to view this cycle as our industrial enterprises essentially lending money to the state with zero interest and infinite maturity.

Especially during periods of high inflation, the issue of outstanding VAT refunds becomes an even greater burden on companies’ cash flow.

The technological transformation of industry has been one of the Istanbul Chamber of Industry’s top strategic priorities in recent years. One year ago, we established the ISO Strategic Transformation Center to guide our industrial sector through this transition. We believe the only way to build a competitive industrial base is to foster a model of technology-driven, export-oriented, and sustainable production.

This chart, which shows the overall structure of industrial production by technology intensity, clearly demonstrates how urgently this transformation is needed. In 2024, the largest share of value added generated within ISO 500 came from the low-tech industries, with 34.6%. It is notable that the share of this group increased by 5.9 percentage points compared to the previous year. While the low-to-medium-tech industries had held the highest share in 2022 and 2023, the renewed dominance of the low-tech industries in 2024 deserves careful attention.

During the same period, the share of the low-to-medium-tech industries fell by 2.5 percentage points to 31.4%, while the medium-to-high-tech industries declined by 3.6 points to 26.7%. The share of high-tech industries rose by 0.3 points and climbed to 7.4 percent.

After reaching a record high of 37.4% in 2023, the combined share of medium-to-high-tech and high-tech industries in the value added generated by ISO 500 fell back to 34.1% in 2024, signaling a loss of momentum.

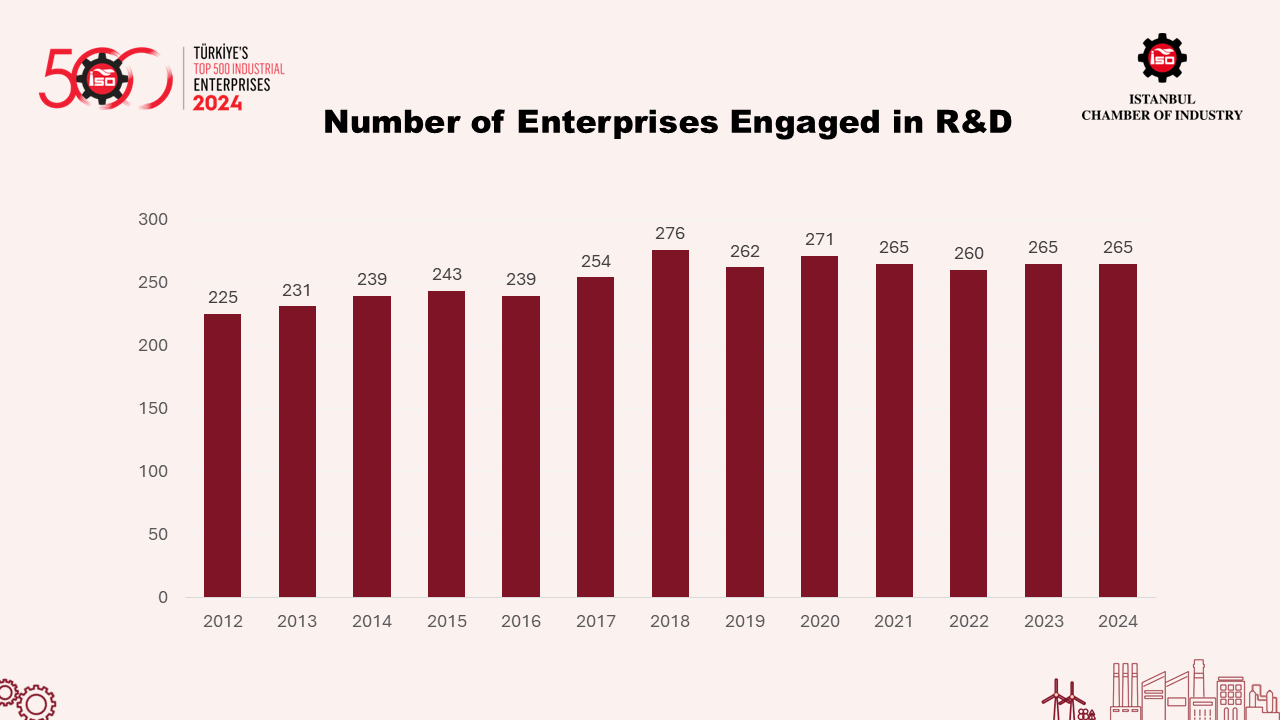

When we examine the number of ISO 500 enterprises investing in R&D, it is evident that our industry needs to show greater enthusiasm in this area. The number of R&D-investing organizations in the ISO 500 appears to have stagnated after a steady increase until 2018.

The number of ISO 500 companies engaging in R&D remained unchanged at 265 in 2024. For the development of a technology-driven and high-value industrial base, industrial enterprises must place greater emphasis on R&D.

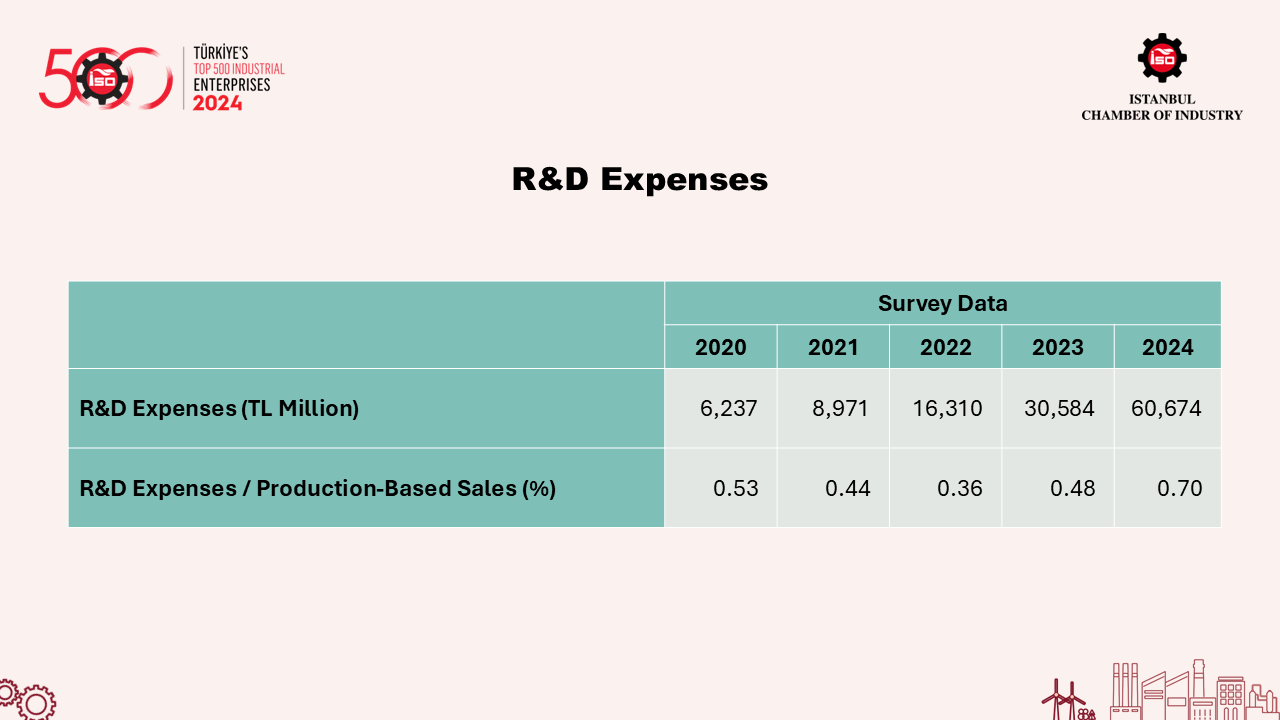

According to ISO 500 survey data, R&D expenditures increased by 98.4% in 2024, reaching TL 60.7 billion. The fact that R&D expenditure as a share of production-based sales reached a high of 0.7% is a promising sign of rising awareness in this area.

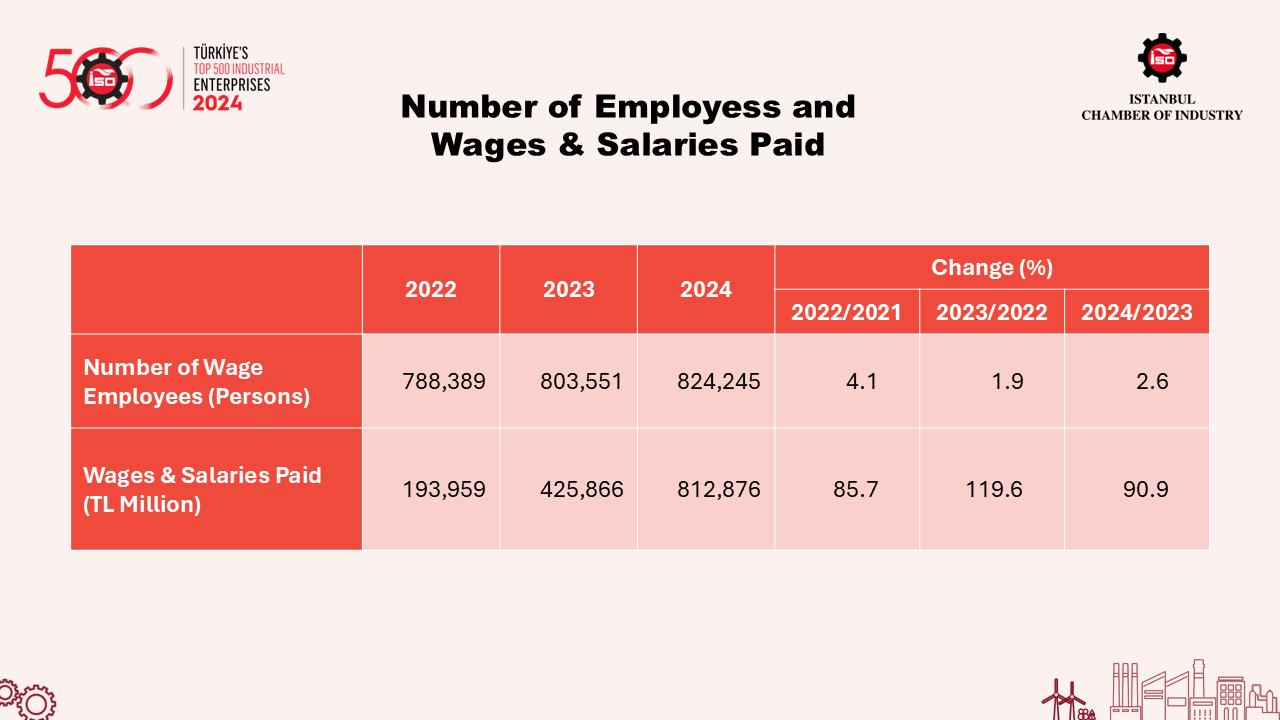

This section presents the employment snapshot for ISO 500 in 2024. The data show that total employment within ISO 500 rose by 2.6%, approaching 825,000 people. In the same year, total salaries and wages paid as full entitlements increased by 90.9% to TL 813 billion.

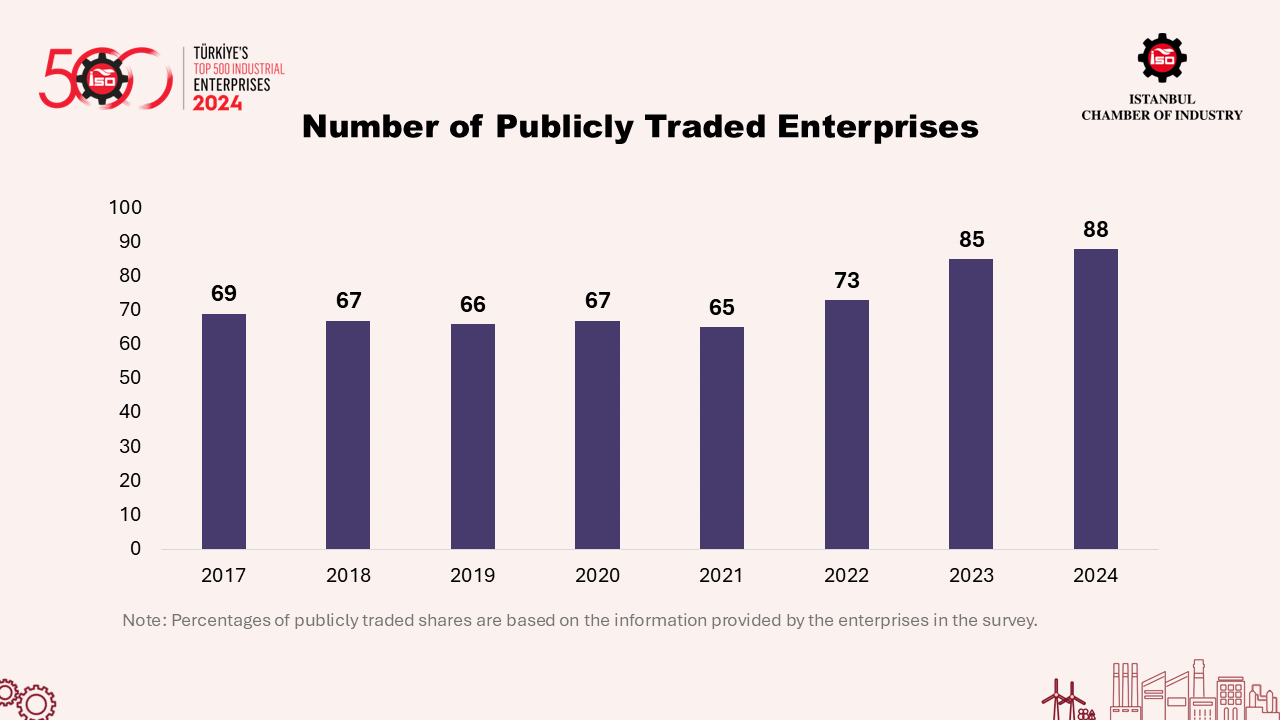

Going public remains an important option for spreading capital more broadly and diversifying industrial companies’ sources of financing. Looking at ISO 500 companies from this perspective, we see that the number of publicly listed firms remained between 65 and 69 during the 2017-2021 period, rising to 73 in 2022 and to 85 in 2023.

This upward trend in publicly traded companies continued in 2024. With three additional companies listed in 2024, the number of publicly traded companies in ISO 500 rose to 88, the highest number recorded to date. We hope to see this trend continue.

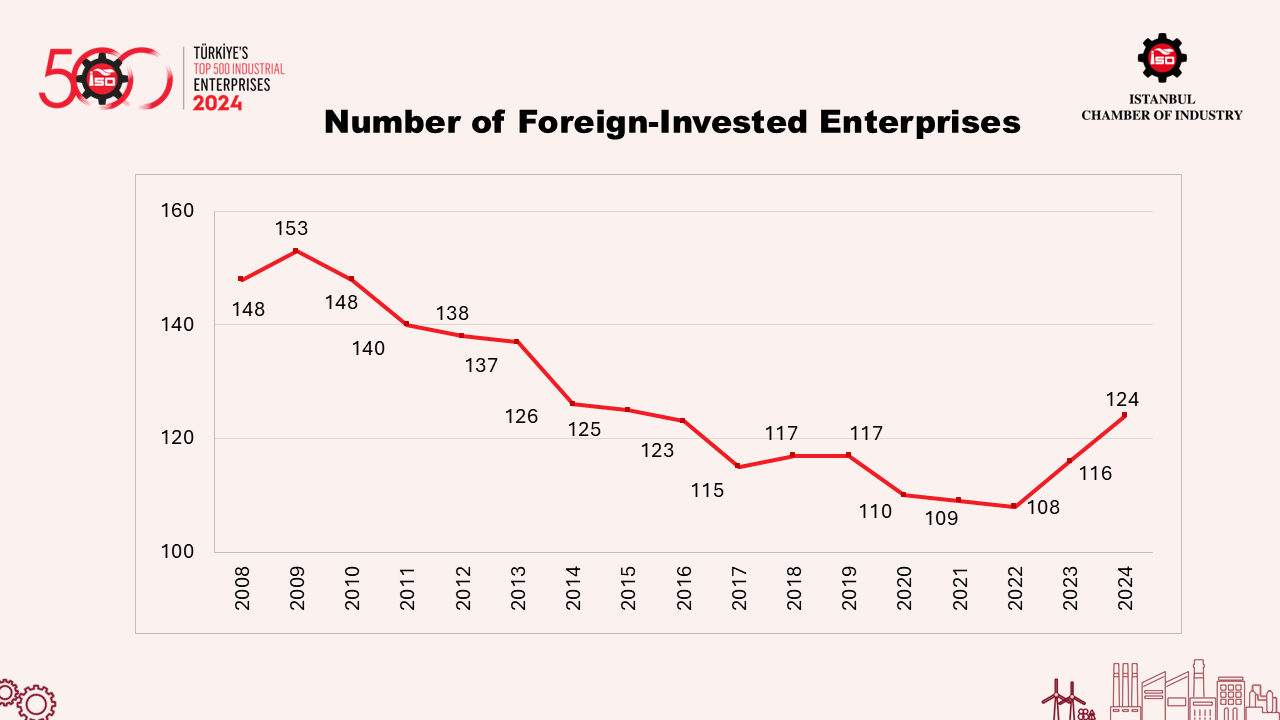

This chart also offers critical insights into the role of foreign capital in Türkiye. We observe that the declining trend in the number of foreign-invested enterprises within ISO 500, which began in the 2010s, was reversed in 2023.

The number of foreign-capital-affiliated companies rose by 8 in 2024, from 116 to 124. As a result, the number of such companies has returned to levels last seen during the 2014-2016 period.

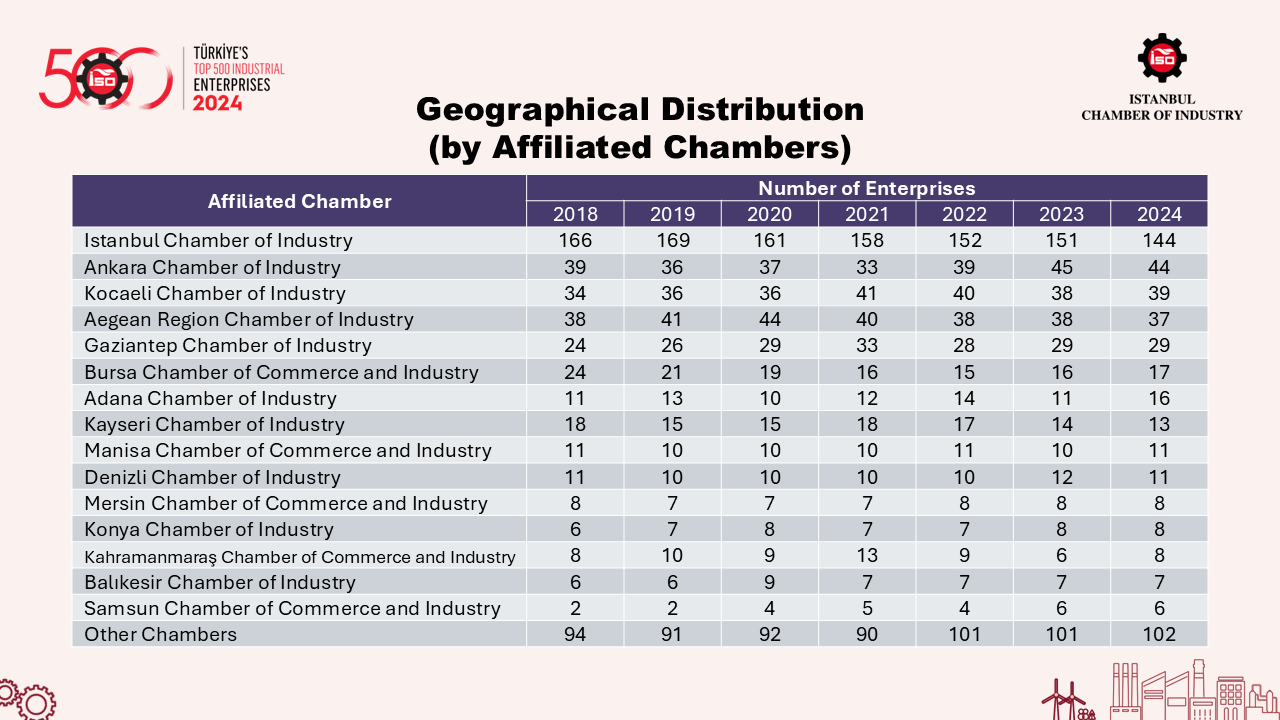

When we rank the ISO 500 according to their respective chambers, we see that the weight of Anatolia continued to increase in 2024.

Although there has been a decrease in numbers in recent years, the largest share belongs to the Istanbul Chamber of Industry, with 144 companies. Following the ICI, the Ankara Chamber of Industry ranks next with 44 enterprises.

Right below, we see the Kocaeli Chamber of Industry with 39 enterprises, which is closely followed by the Aegean Region Chamber of Industry with 37 enterprises. The following are the Gaziantep Chamber of Industry with 29 organizations, Bursa Chamber of Commerce and Industry with 17, and Adana Chamber of Industry with 16.

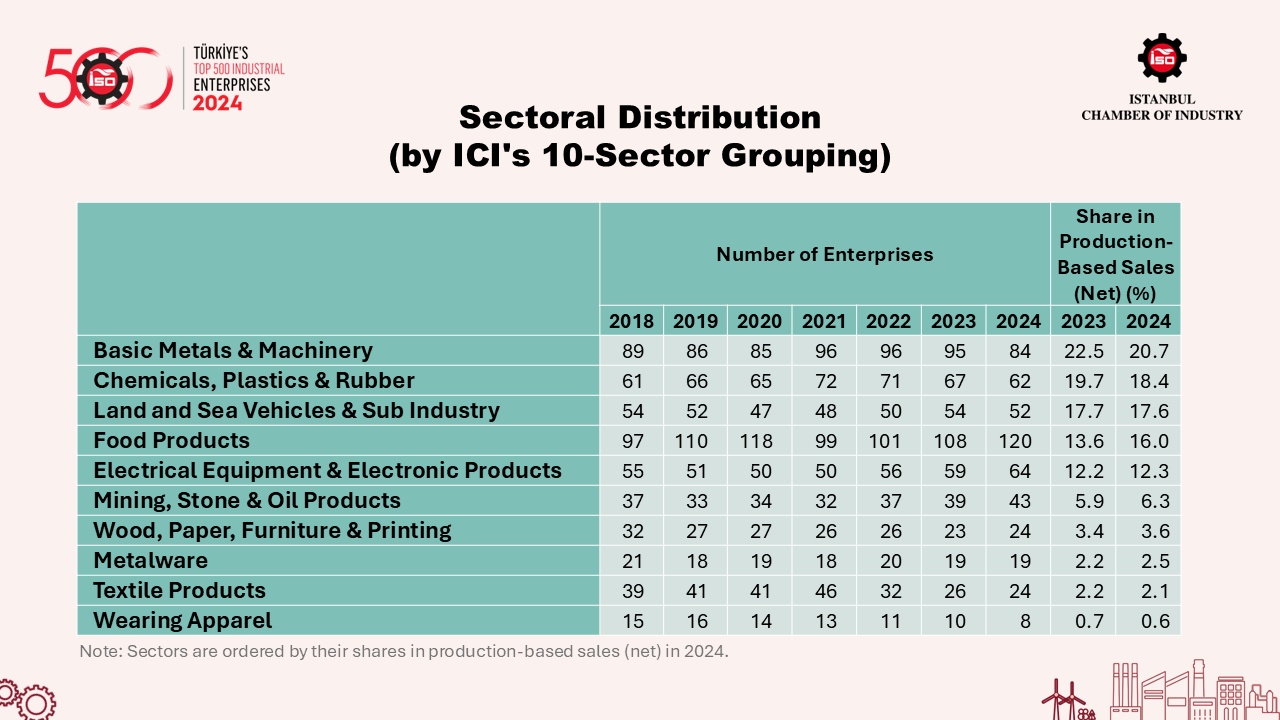

When examining the sectoral breakdown of the ISO 500, we discern the following distribution based on the 10-sector categorization formulated by our Chamber:

In 2024, the sector with the highest share of production-based sales was the "manufacture of basic metals and machinery" at 20.7 percent, though this share fell by 1.8 percentage points from last year.

The "manufacture of chemical, plastic, and rubber products", ranking second at 18.4 percent, saw a decline of 1.3 percentage points from the previous year.

In third place, despite a very slight decrease in its share compared to the previous year, is once again the “land vehicles, marine vehicles, and related sub-industries” group, with a share of 17.6%.

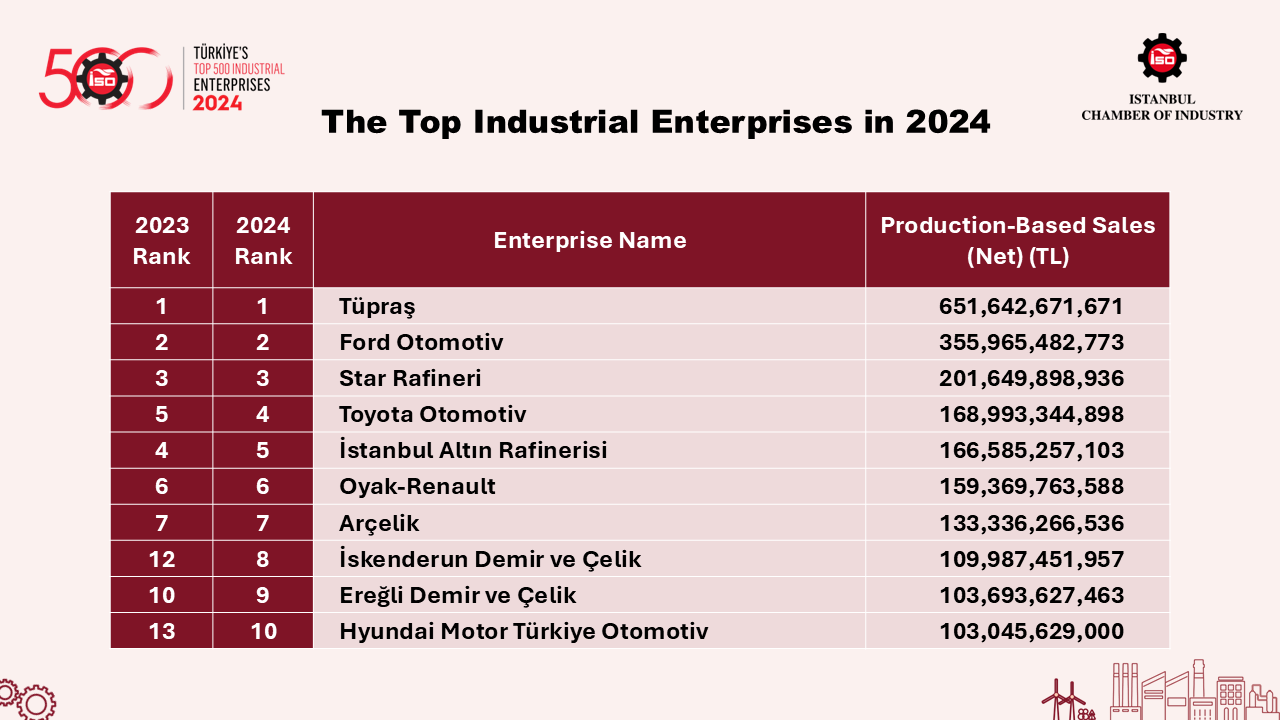

And now we arrive at the most anticipated part of the ISO 500 report, the ranking based on production-based sales. As in previous years, TÜPRAŞ was once again the largest company in ISO 500 in 2024, with production-based sales of TL 651.6 billion.

In second place was Ford Otomotiv Sanayi A.Ş. with TL 356 billion, followed by Star Rafineri A.Ş. in third place with TL 201.6 billion. Notably, both companies have maintained their rankings from the previous year. Accordingly, the top three spots in ISO 500 remained unchanged compared to last year.

However, two changes occurred among the top 10 ISO 500 companies in 2024 compared to 2023. İskenderun Demir Çelik and Hyundai Motor Türkiye Otomotiv, which were not in the top ten last year, succeeded in entering the top 10 this year.

Distinguished Members of the Press,

Esteemed Guests,

The ISO 500 data clearly demonstrate that our country is at risk of drifting into a cycle of deindustrialization. It is in our hands to break and reverse this trend.

And this responsibility should not rest solely on the shoulders of industrialists; it must be shared by all. Because in this era of rising global tensions and protectionism, the industrial sector and production are of vital importance for Türkiye. Before Türkiye falls deeper into the cycle of deindustrialization, we must firmly adopt technology-driven, export-oriented, and high-quality production as the foundation for competitive, sustainable growth and prosperity.

Moreover, in our region, surrounded by geopolitical tensions, a strong industrial infrastructure is also vital for the country’s resilience and defense in every sense.

In this regard, we eagerly await the recently announced “2030 Industry and Technology Strategy,” which was built around five key objectives set by the Presidency: High Technology, Digital Economy, Green Transformation, Global Integration, and Structural Transformation. We believe this strategy reflects the vision our industry needs most. I would also like to state that the work of our ISO Strategic Transformation Center will take this new presidential strategy as a guiding framework.

In closing, as we always emphasize at the Istanbul Chamber of Industry, we must continue to work tirelessly for a model of holistic development that earns its reputation not from consumption but from production. Thank you again for your interest in today’s meeting, and I extend my warmest regards on behalf of ISO.

EN

EN