Following the announcement of the 2024 “Türkiye’s Top 500 Industrial Enterprises (ISO 500)” survey in May, the Istanbul Chamber of Industry (ICI) has today shared the results of its “Türkiye’s Second Top 500 Industrial Enterprises (ISO Second 500)” survey, which covers smaller and medium-sized enterprises compared to those in the ISO 500.

As in previous years, the ISO Second 500 survey has provided important insights into the development of smaller and medium-sized enterprises in terms of the economic and financial conditions they face, their export performance, employment, R&D, and technological activities.

Undoubtedly, while evaluating these results, it is essential to take into account the impact of global economic fragility and uncertainties, as well as the effects of tight monetary policies implemented domestically, on the industrial enterprises.

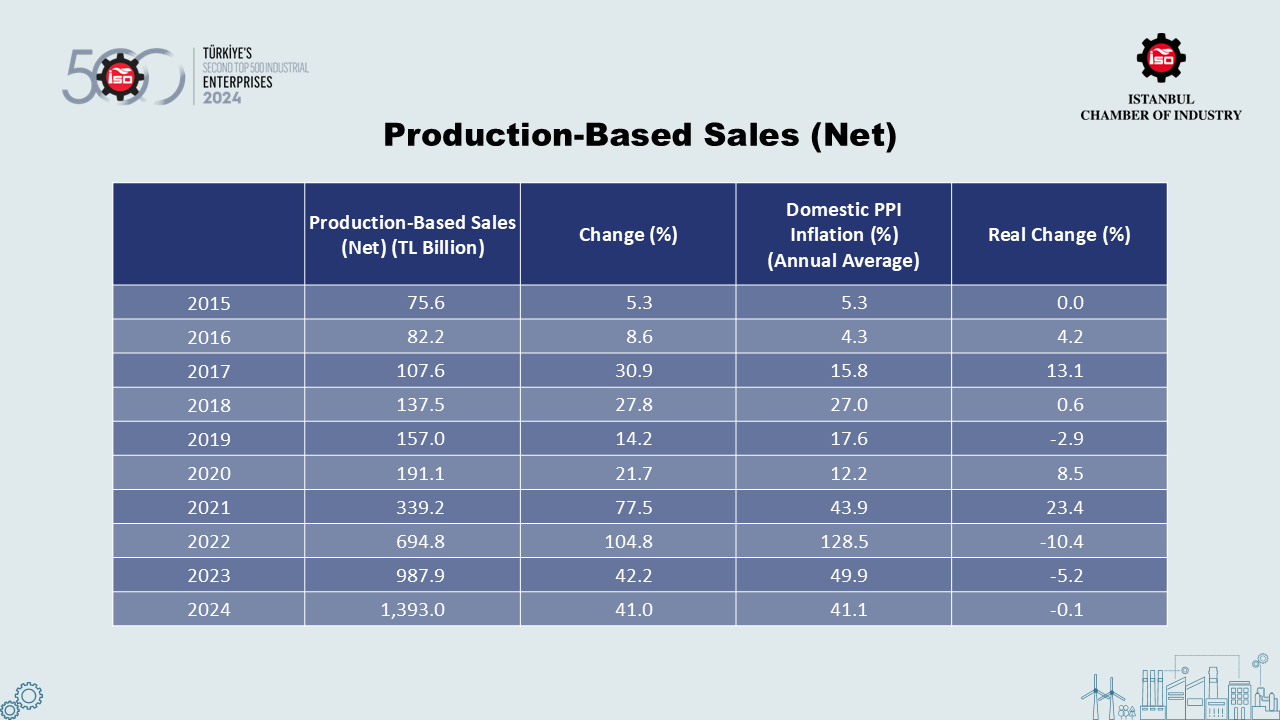

The main ranking criterion – and also one of the most important indicators – of the ISO Second 500 is “net production-based sales.” Looking at the results for 2024, ISO Second 500 companies increased their production-based sales from TL 988 billion to TL 1.393 trillion. This 41 percent growth performance remained below the levels observed over the past three years.

When adjusted for the 2024 annual average Domestic Producer Price Index (D-PPI), which stood at 41.1 percent, production-based sales actually declined in real terms by 0.1 percent. Thus, as was the case with the ISO 500, the downward trend in real production-based sales – recorded at 10.4 percent in 2022 and 5.2 percent in 2023 – continued for the third consecutive year.

Both domestic and international developments played a decisive role in this weak performance in 2024. Domestically, tighter monetary policies began to be implemented more comprehensively as of April 2024. As a result, the gradual slowdown in domestic demand had a negative impact on sales in the industrial sector.

On the external front, weak demand in export markets throughout 2024, the inability to fully reflect rising cost pressures in sales prices, the trend of real appreciation in the Turkish lira, and the negative cross-currency effect caused by a strong U.S. dollar all contributed to a decline in the international competitiveness of the industrial sector, weakening its overall sales performance.

Top Three Companies in the ISO Second 500

According to the 2024 ISO Second 500 ranking based on production-based sales, İstanbul Asfalt Fabrikaları secured the top spot with TL 4.186 billion. It was followed by Yılmaz Redüktör with TL 4.185 billion, while Boyteks Tekstil ranked third with TL 4.169 billion.

To be included in the 2024 ISO Second 500 list, companies needed to have production-based sales between TL 4.186 billion and TL 1.820 billion. In comparison, companies on the 2023 list had production-based sales ranging from TL 2.958 billion to TL 1.294 billion.

A total of 66 new enterprises entered the ISO Second 500 ranking in 2024. Forty-one companies, that were included in the ISO 500 in the study of 2023, moved down to the ISO Second 500 in 2024. Meanwhile, 393 companies were featured on the ISO Second 500 list in both 2023 and 2024.

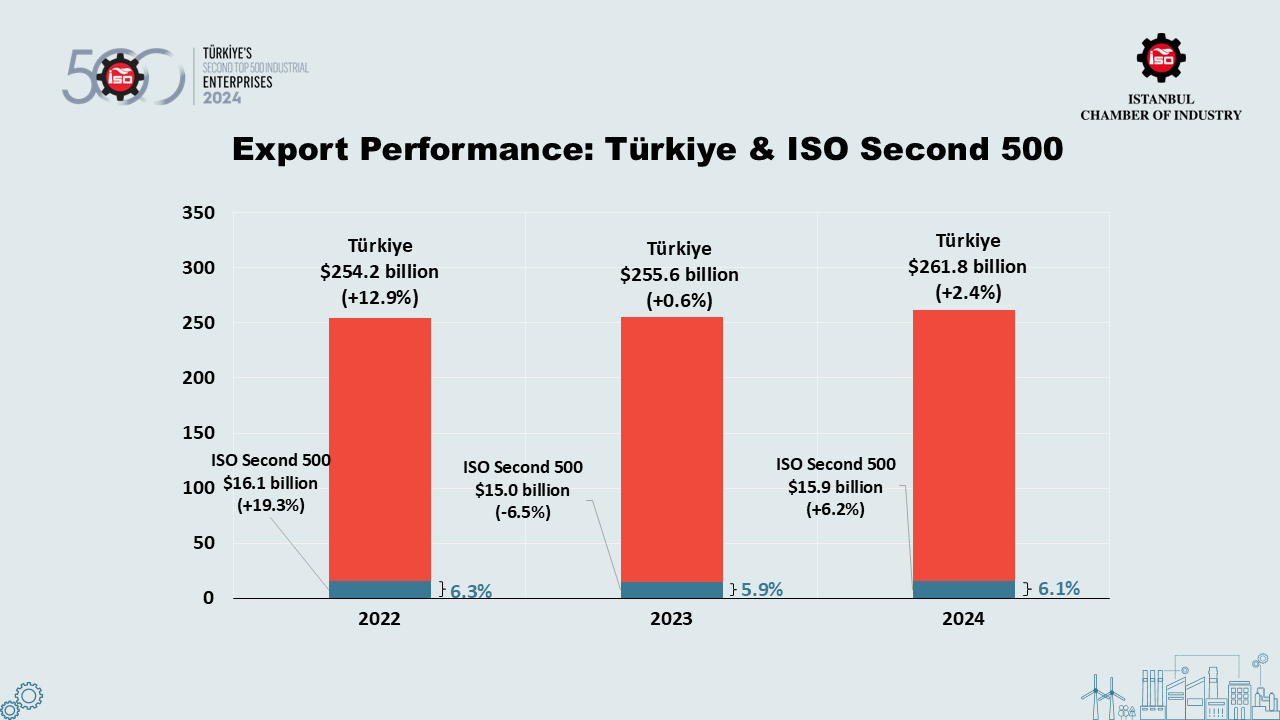

Despite weakened global demand conditions in 2024, Türkiye’s exports rose moderately by 2.4 percent, reaching USD 261.8 billion, while exports from the industrial sector increased by 2.6 percent to USD 252.1 billion. Exports of the ISO Second Top 500 rose by 6.2 percent, reaching USD 15.9 billion.

The ISO Second 500 outperformed the ISO 500 in terms of export growth. This was largely due to the strong export performance of the textile and apparel sectors, which have a greater weight in terms of the number of firms within the ISO Second 500.

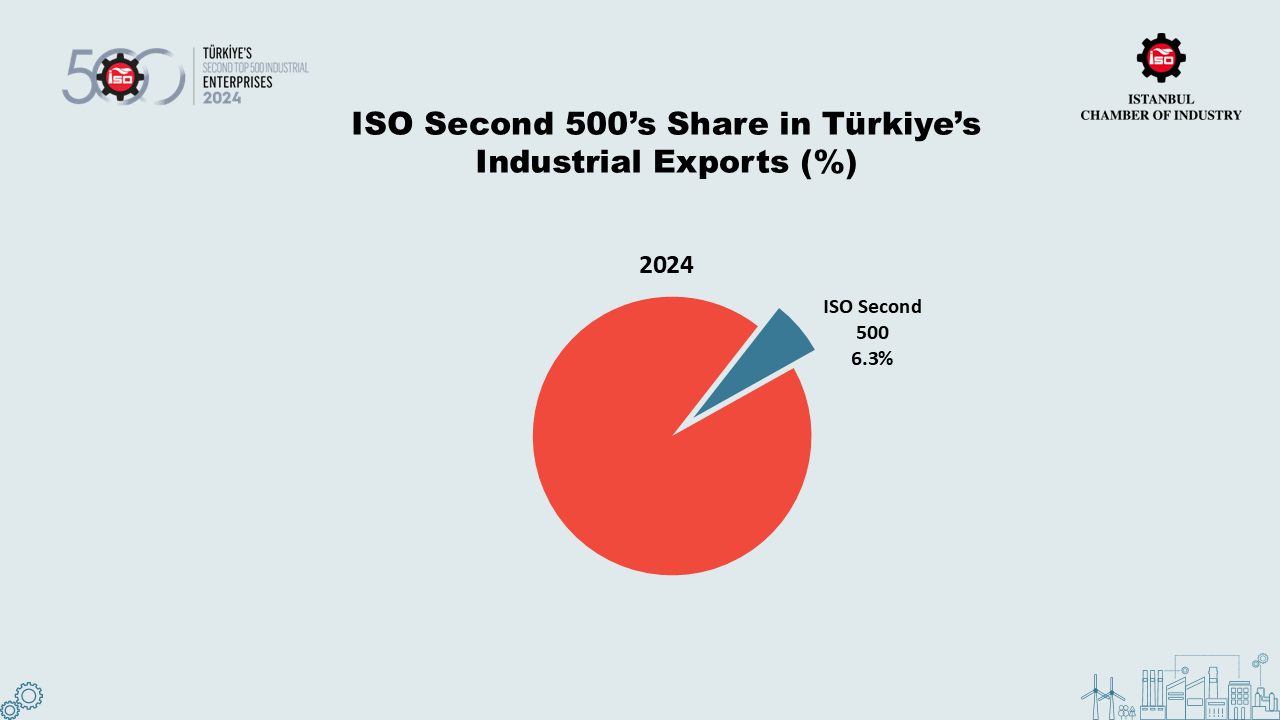

As a result, the share of the ISO Second 500 in Türkiye’s industrial exports increased to 6.3 percent in 2024, up by 0.2 percentage points.

As was the case with the ISO 500, profits in the ISO Second 500 also showed sharp declines in 2024. In addition to weak sales performance, significant increases in costs affected operating profitability negatively.

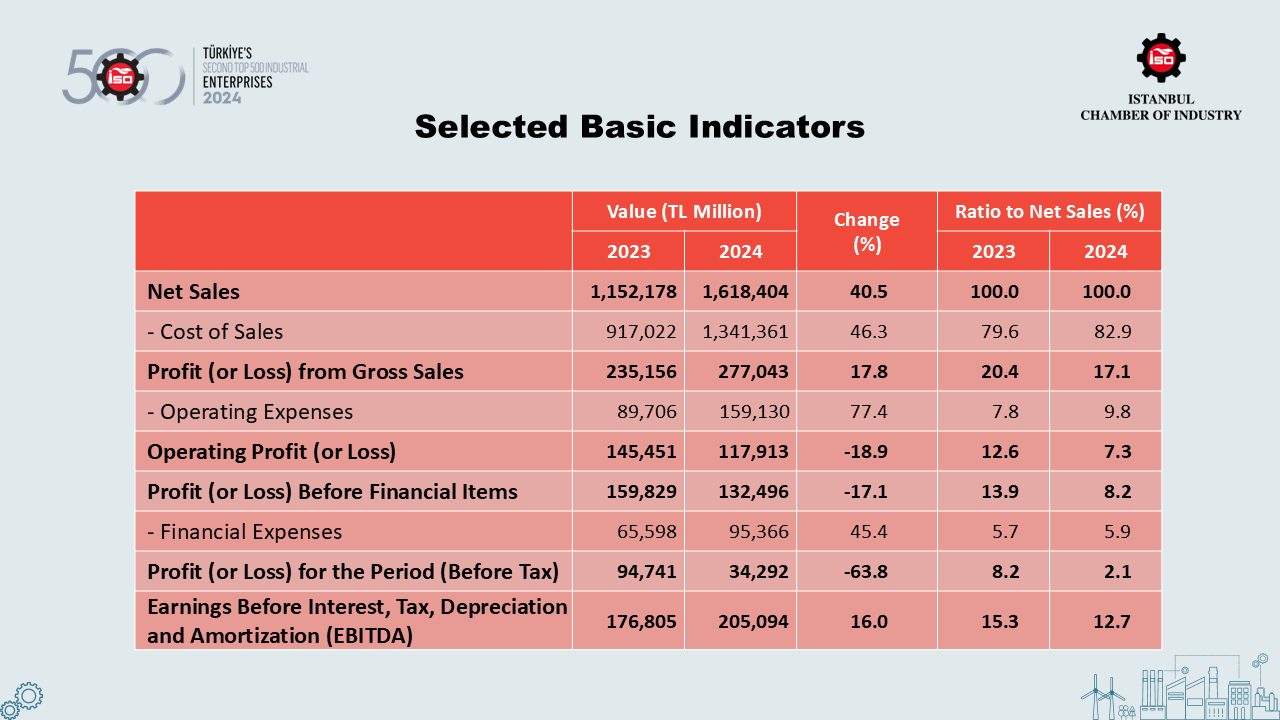

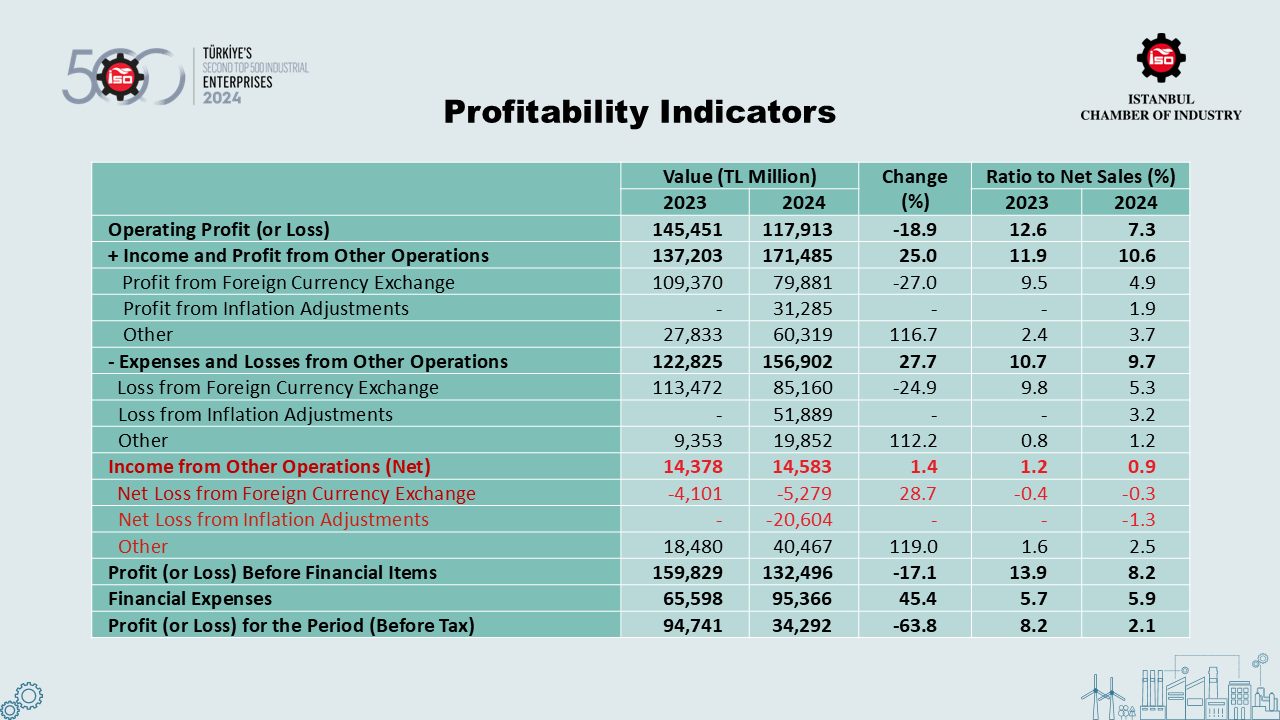

The operating profit of the ISO Second 500 decreased by 18.9 percent in 2024, falling from TL 145 billion to TL 118 billion. Accordingly, the operating profit margin dropped from 12.6 percent to 7.3 percent. This was significantly below the 2014-2023 average of 10.9 percent.

The total profit and loss before tax of the ISO Second 500 declined by 63.8 percent in 2024, from TL 95 billion to TL 34 billion. The sales profitability ratio also fell from 8.2 percent to 2.1 percent, remaining well below its ten-year average of 7 percent.

The decline in pre-tax profit and loss was partly due to a net inflation adjustment loss of TL 20.6 billion resulting from the application of inflation accounting. This loss reduced sales profitability by 1.3 percentage points. Without this adjustment, the ISO Second 500’s sales profitability would have been 3.4 percent instead of 2.1 percent.

Another key profitability indicator, earnings before interest, tax, depreciation, and amortization (EBITDA), rose modestly by 16 percent, increasing from TL 177 billion to TL 205 billion. Since this growth lagged behind that of net sales, the EBITDA margin decreased by 2.6 percentage points, from 15.3 percent to 12.7 percent. This rate was below the 2014-2023 average of 13.8 percent.

In 2024, a negative picture emerged across all profitability indicators of the ISO Second 500.

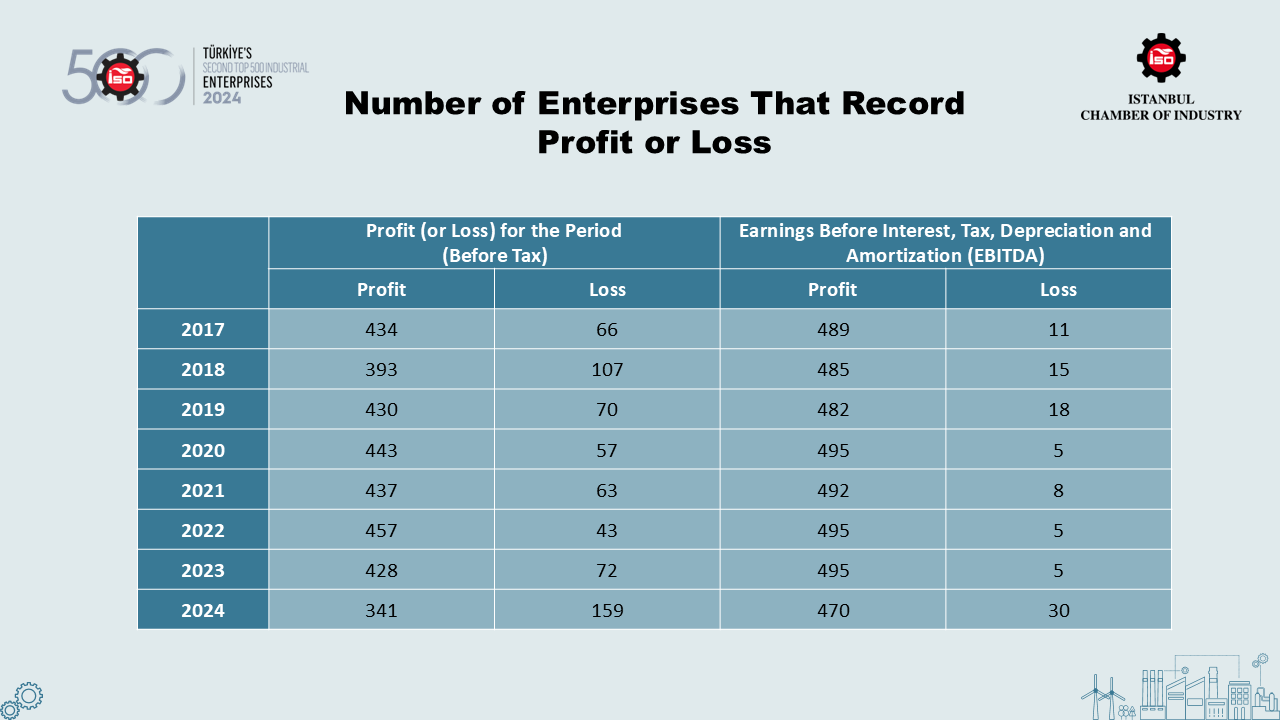

Weak performance in profitability was also clearly reflected in the number of profit- and loss-making companies.

Based on pre-tax profit and loss figures, the number of profitable companies in the ISO Second 500 decreased from 428 in 2023 to 341 in 2024. Meanwhile, the number of loss-making companies rose from 72 to 159. This figure stands out as the highest since the ISO Second 500 rankings began to be published in 1997.

On the other hand, when considering earnings before interest, taxes, depreciation, and amortization (EBITDA) as the basis for operational profitability, the number of profitable companies declined from 495 to 470, while the number of loss-making companies increased to 30, the highest since 2013.

When comparing the profitability components of the ISO Second 500 with the previous year, it is seen that, as in 2023, a net foreign exchange loss occurred in 2024. In the same year, a net adjustment loss also arose due to the implementation of inflation accounting.

In 2024, ISO Second 500 companies generated a net profit of TL 40 billion from non-operating income excluding foreign exchange and inflation adjustments. The ratio of this figure to net sales increased from 1.6 percent to 2.5 percent.

Non-operating income includes many items such as interest income, dividend income from affiliates and subsidiaries, gains and losses from securities, sales of fixed assets, commissions, etc.

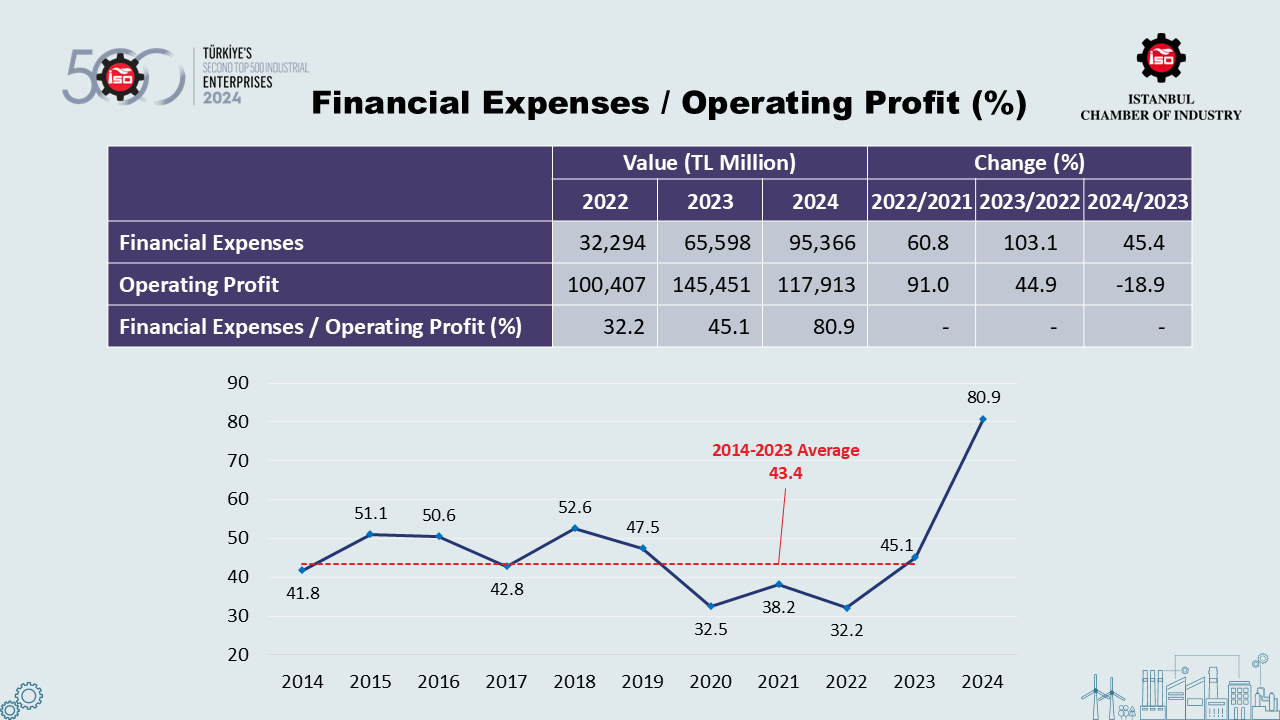

As in previous years, financing expenses continued to be one of the key determinants of profitability for industrial companies in both the ISO 500 and the ISO Second 500 in 2024.

Financing expenses of the ISO Second 500 increased by 45.4 percent, reaching TL 95 billion. In the same year, operating profit decreased by 18.9 percent to TL 118 billion. As a result, the ratio of financing expenses to operating profit rose sharply by 35.8 percentage points to 80.9 percent.

Given that the average of this ratio was 43.4 percent between 2014 and 2023, industrialists are now allocating not just half, but more than four-fifths of their operating profits to financing expenses – a long-standing concern that has now become a reality.

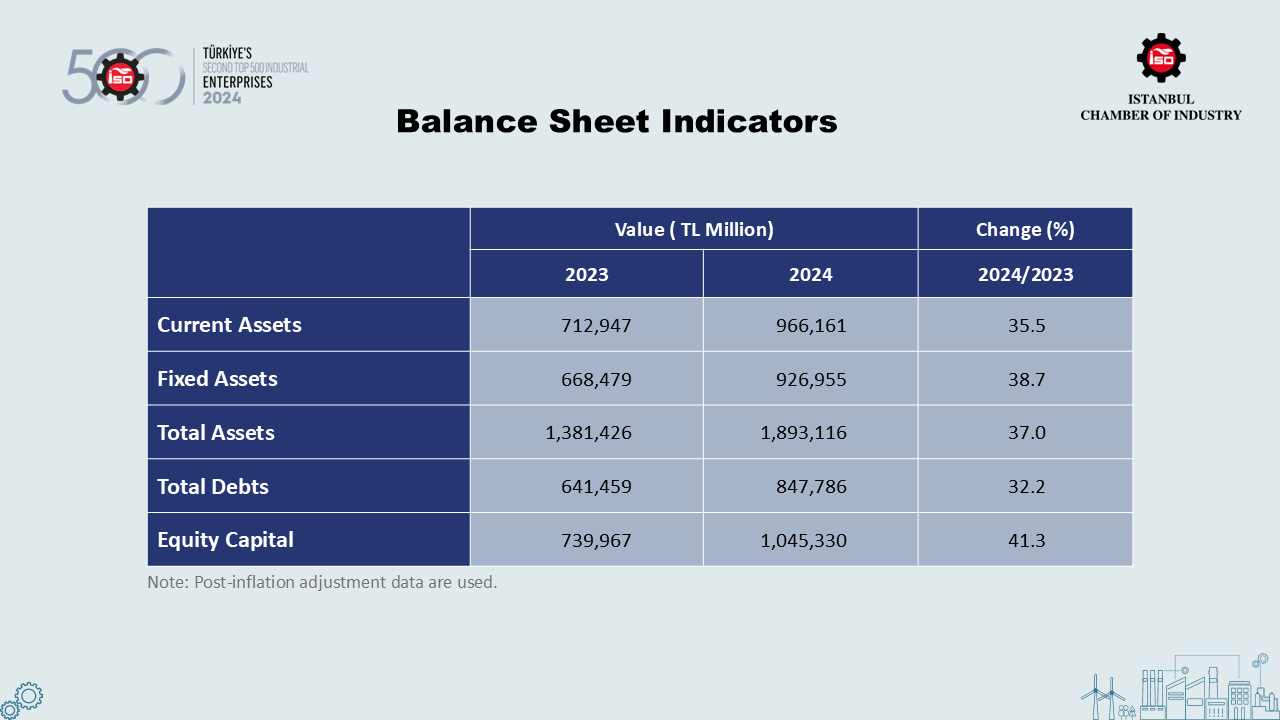

As is well known, the implementation of inflation accounting in 2023 led to significant increases in balance sheet items, particularly in assets and equity. An analysis of ISO Second 500 companies shows that the impact of inflation adjustments was more limited in 2024.

The data indicates that current assets grew by 35.5 percent and fixed assets by 38.7 percent, resulting in a 37 percent increase in total assets.

On the liabilities side, shareholders’ equity rose by 41.3 percent, while total debt increased by a lower rate of 32.2 percent. This shows that, as in 2023, equity grew faster than assets in 2024 as well.

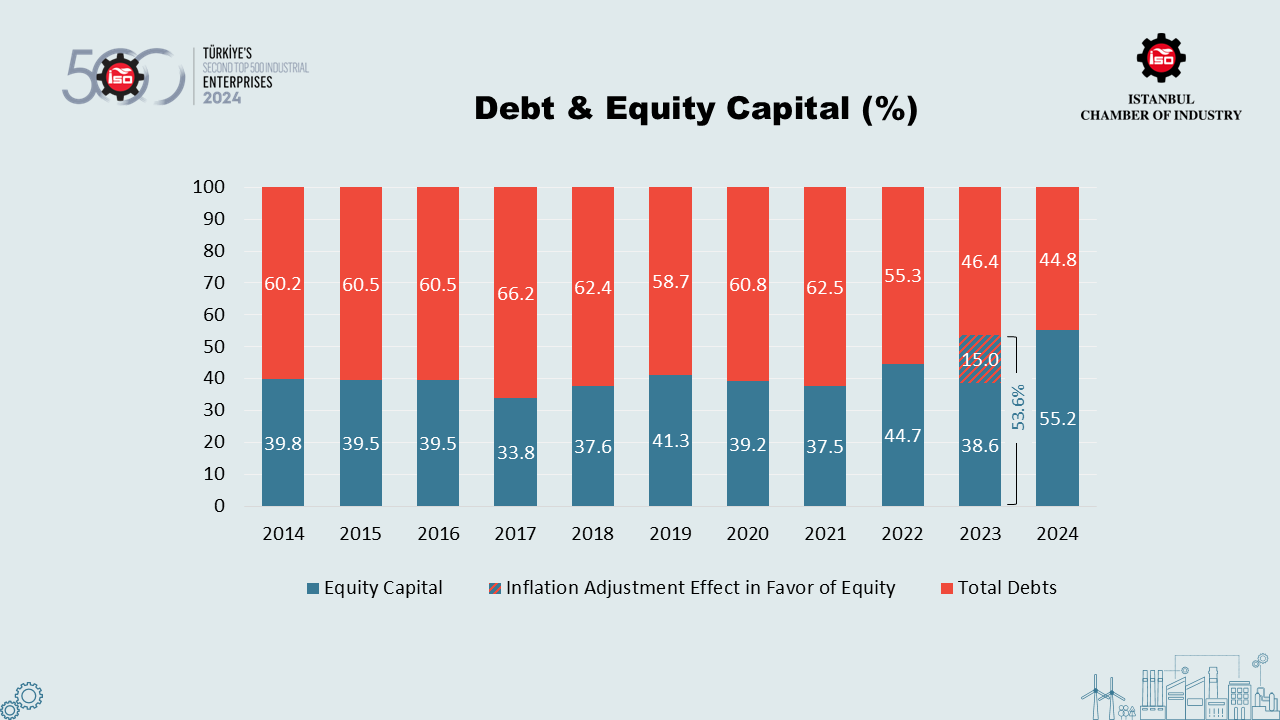

The ISO Second 500 also provides striking data regarding the distribution of debt and equity. As a reminder, the inflation adjustment implemented in 2023 primarily affected the capital structure of the ISO Second 500 through equity and played a role in improving the funding composition.

In 2024, the shift in the capital structure once again appears to have favored equity. The share of equity in total assets increased from 53.6 percent in 2023 to 55.2 percent in 2024, while the share of total debt declined from 46.4 percent to 44.8 percent.

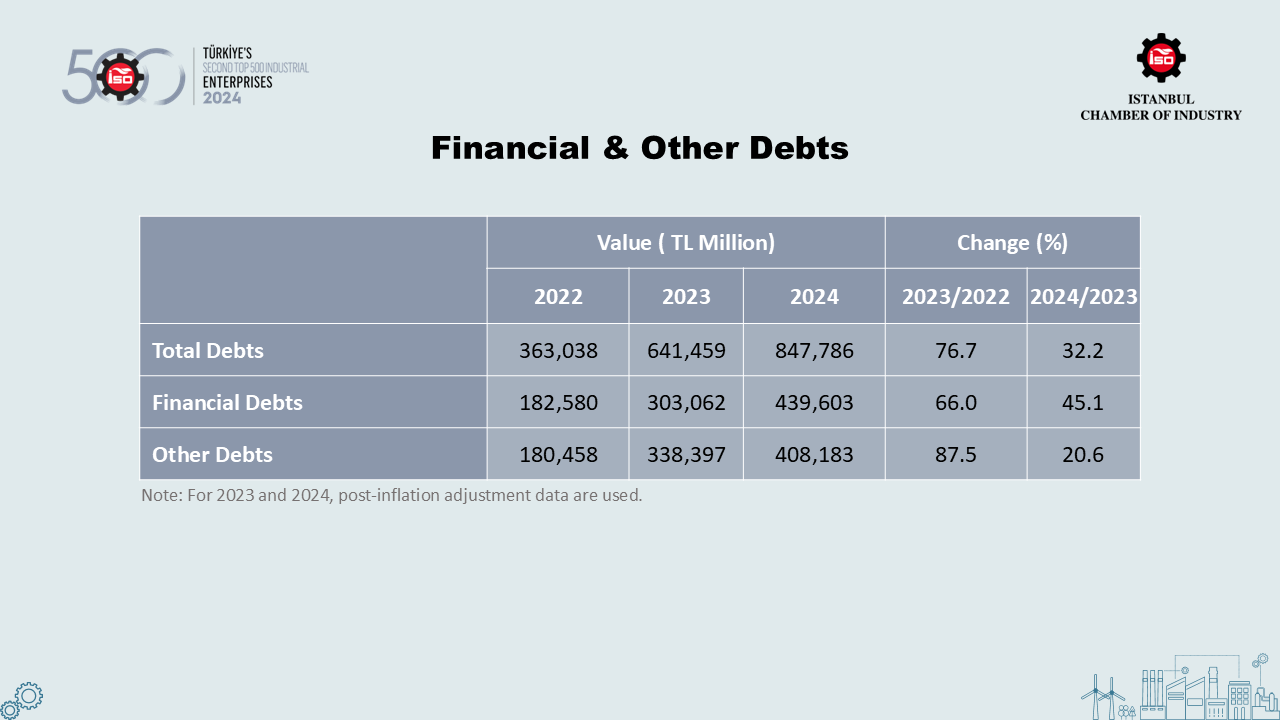

In the ISO Second 500, total debt increased by 32.2 percent in 2024, following a 76.7 percent rise in 2023. Looking at the subcategories, the increase in financial debts, which was 66 percent in 2023, slowed to 45.1 percent in 2024. Other debts grew by only 20.6 percent in 2024, a sharp slowdown compared to the 87.5 percent increase recorded in the previous year.

In contrast to the previous three years, financial debts grew more than other debts in 2024. This indicates that, despite rising interest rates, relatively smaller and medium-sized enterprises still had to rely on bank loans to meet their financing needs.

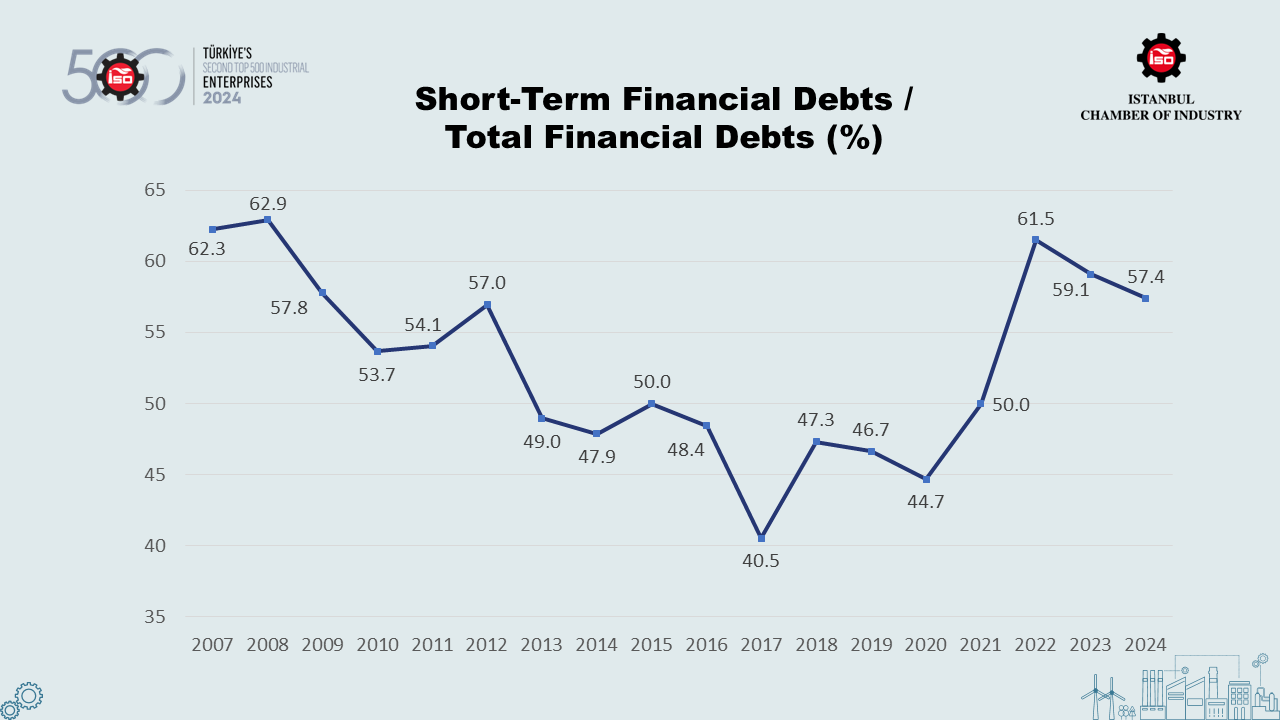

In terms of the maturity composition, the slowdown in the growth of short-term financial debts is particularly noteworthy. This trend is also reflected in the share of short-term financial debts within total financial debts.

Specifically, after increasing in 2021 and 2022, the share of short-term financial debts declined to 59.1 percent in 2023 and further to 57.4 percent in 2024, partly due to the impact of tight monetary policies that constrained short-term borrowing opportunities. Nevertheless, these ratios remain significantly high compared to 2021 and earlier levels.

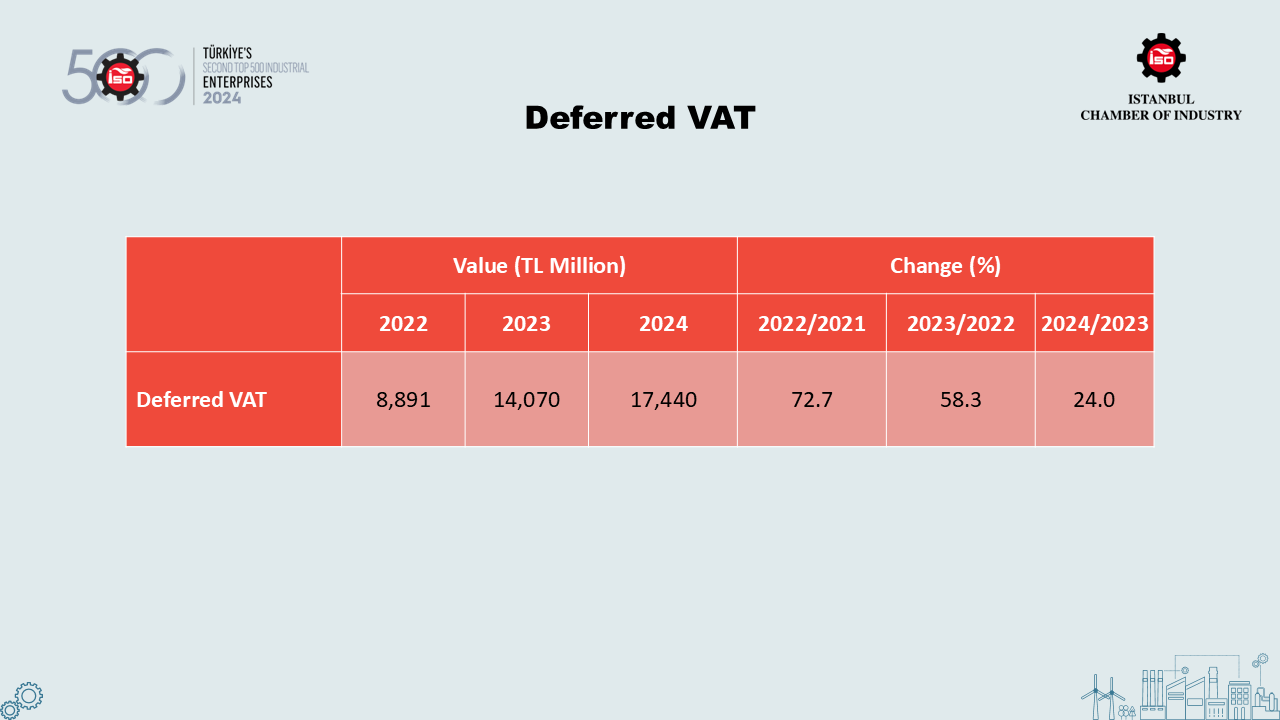

The issue of deferred VAT receivables, which industrialists have long voiced and proposed various solutions for, remains unresolved for both the ISO 500 and ISO Second 500 companies.

As may be recalled, the amount of deferred VAT for ISO 500 rose by 26.9 percent in 2024, reaching nearly TL 84.7 billion. In the ISO Second 500, the amount increased by 24 percent year-on-year, reaching TL 17.4 billion.

Although this increase represents a relatively more positive picture compared to previous years – given that it remained below the inflation rate – it is important to note that industrialists have long perceived this situation as effectively providing the state with an interest-free and indefinite-term loan.

Especially in periods of high inflation, the problem of deferred VAT becomes an even heavier burden on the cash flows of industrial companies.

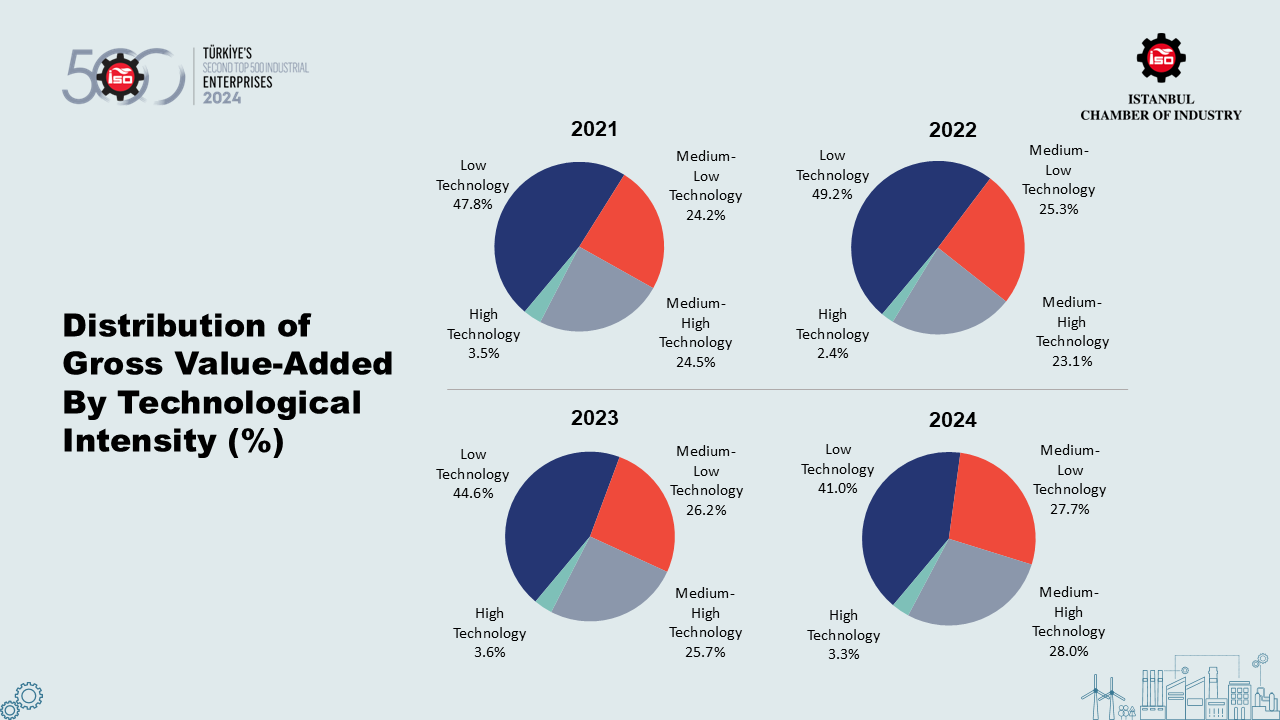

Another noteworthy indicator in the ISO Second 500 is the distribution of value-added by technology intensity. According to the data, the highest share once again belongs to low-tech industries, accounting for 41 percent. However, this represents a 3.6-point decrease compared to the previous year.

In contrast, the share of medium-low-tech industries increased by 1.5 points to reach 27.7 percent, while the share of medium-high-tech industries rose by 2.3 points to 28 percent.

The share of high-tech industries, on the other hand, declined by 0.3 points, falling to 3.3 percent.

Although these figures indicate that, for the first time, the combined share of medium-high- and high-tech industries in the ISO Second 500 has surpassed the 30 percent threshold, it is clear that this level remains insufficient. In a future where digitalization and green transformation will shape global competitiveness, industrialists must intensify their efforts in this area.

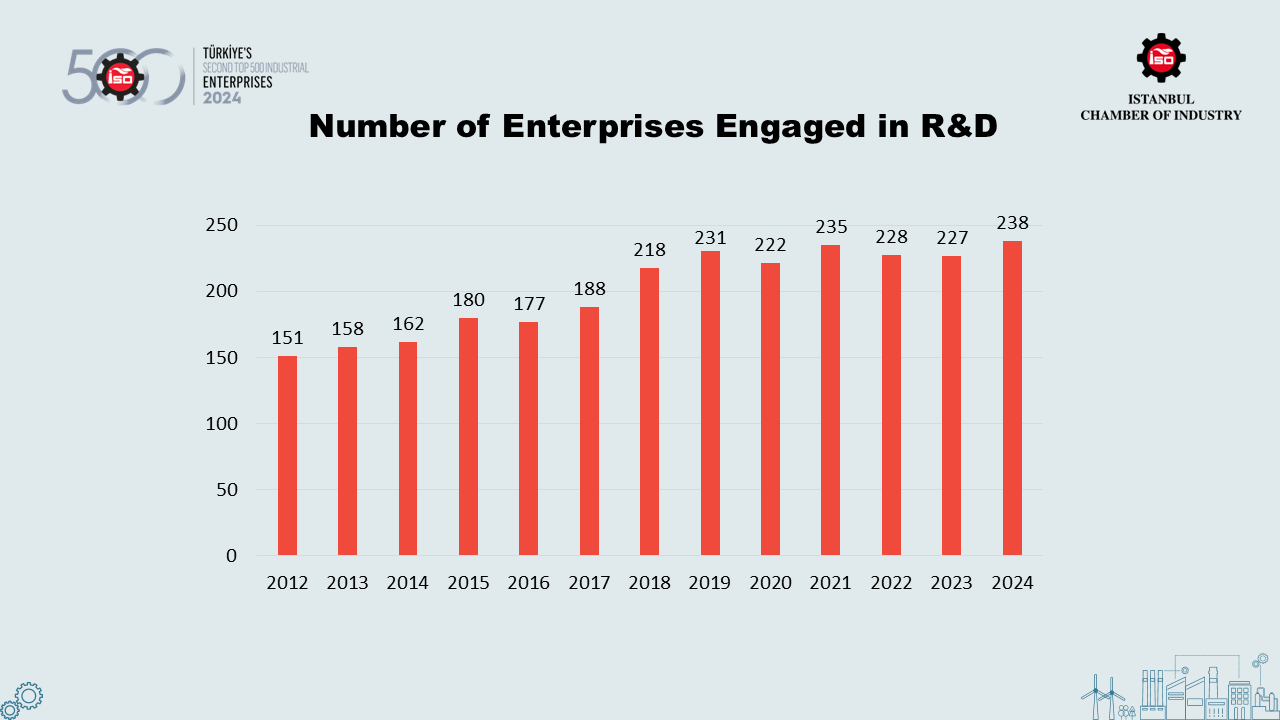

R&D activities remain critically important for the competitiveness of the industrial sector. After a period of stagnation in recent years, the number of companies engaged in R&D in the ISO Second 500 increased by 11 in 2024, reaching 238 – the highest level to date.

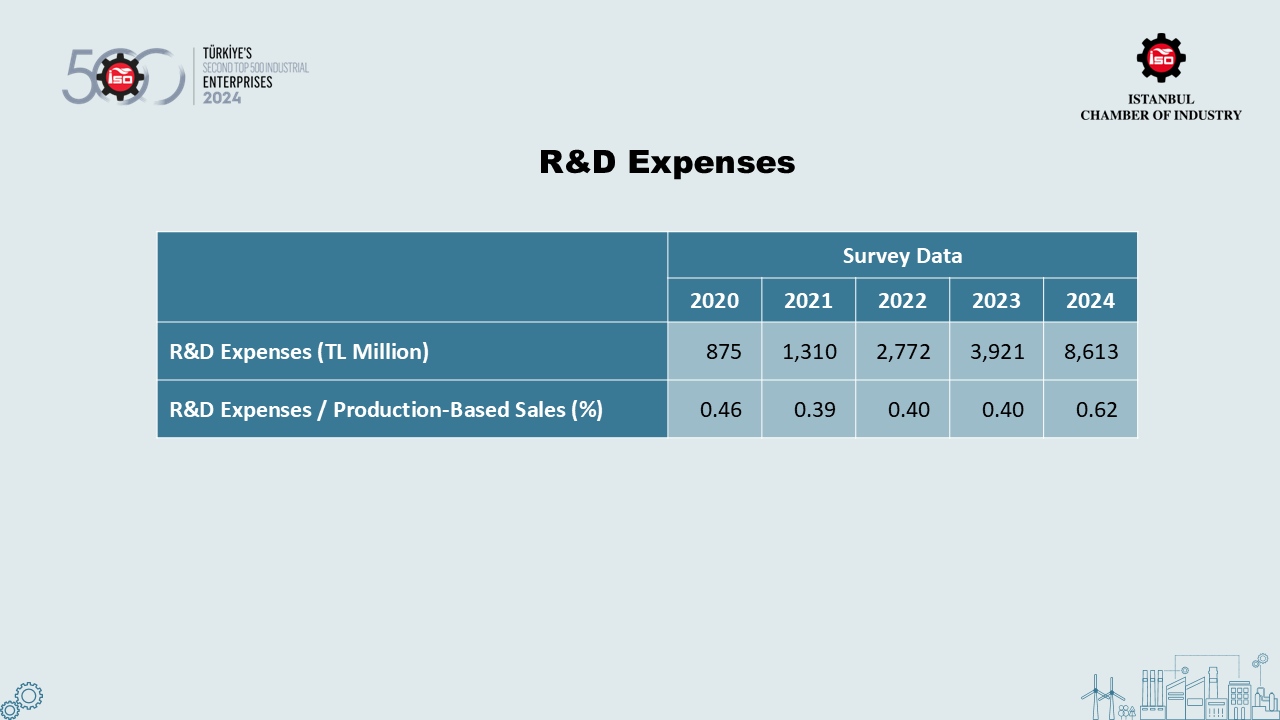

Alongside the rise in companies involved in R&D, total spending by the ISO Second 500 on these activities amounted to TL 8.6 billion in 2024 according to survey data. This represents a 120 percent increase compared to the TL 3.9 billion spent in 2023.

The ratio of R&D expenditure to production-based sales also reached its highest level at 0.62 percent. For a technology-driven, high-quality, and value-added industrial structure, it is essential that our companies place greater emphasis on R&D.

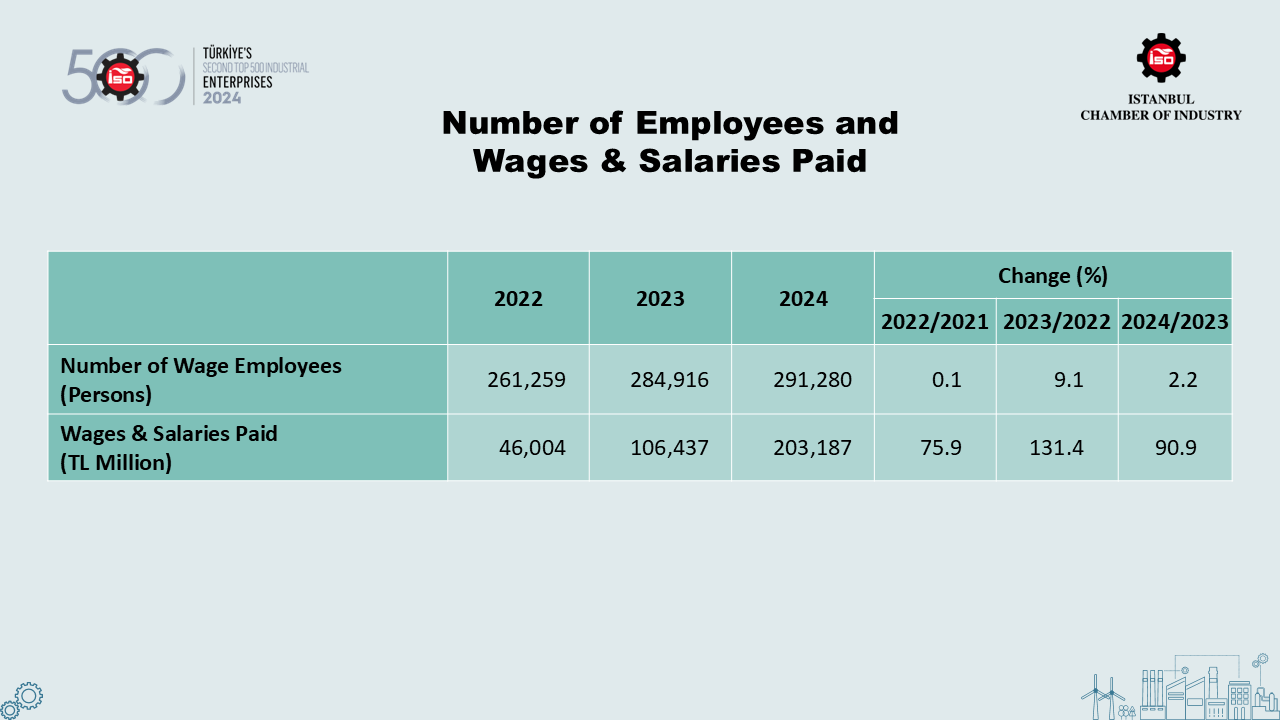

In 2024, a year in which the overall increase in industrial employment in Türkiye remained limited, employment in the ISO Second 500 rose by 2.2 percent, exceeding 291,000 people. In the same year, the increase in wages and salaries paid was 90.9 percent, significantly outpacing inflation.

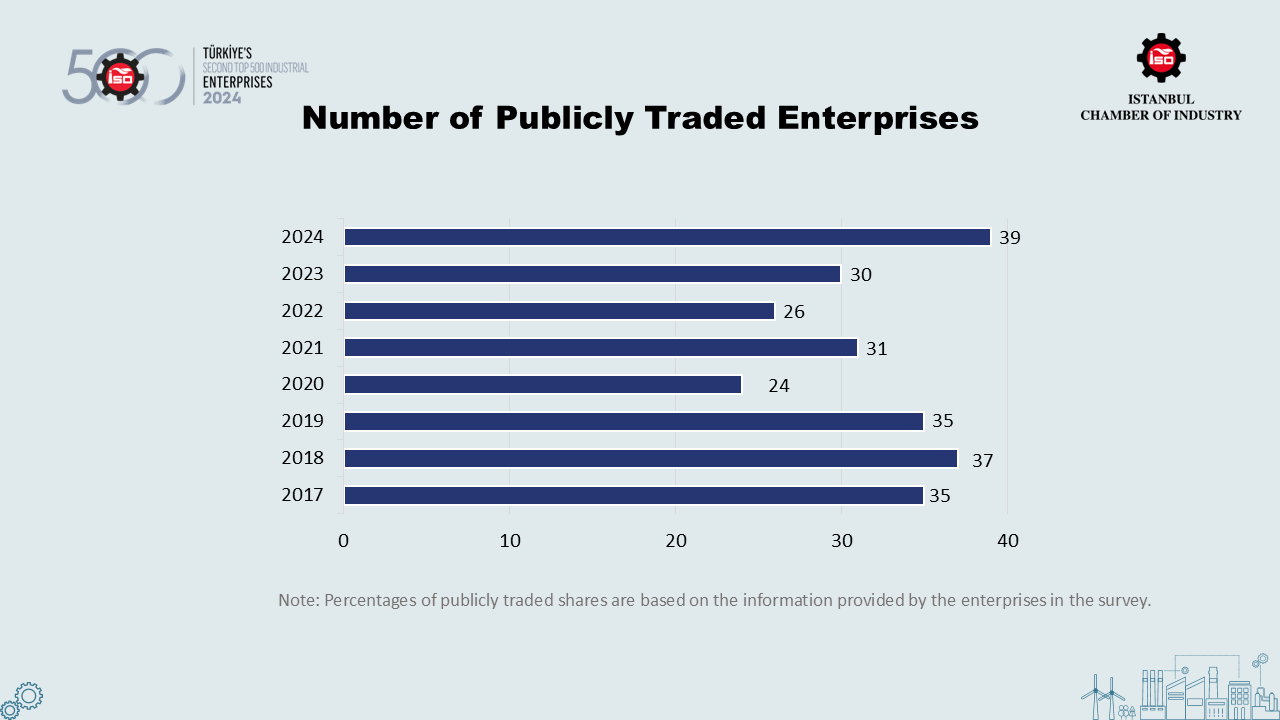

After fluctuating between 2017 and 2023, the number of publicly traded companies in the ISO Second 500 continued to rise 2024. Following an increase of 4 to reach 30 companies in 2023, the number grew by a further 9 in 2024, reaching a record high of 39.

Public listings are important for broadening the shareholder base and, especially, for industrial companies' access to quality financing sources. The increase in the number of publicly traded companies within the ISO 1000 indicates a strengthening trend toward going public in the industrial sector.

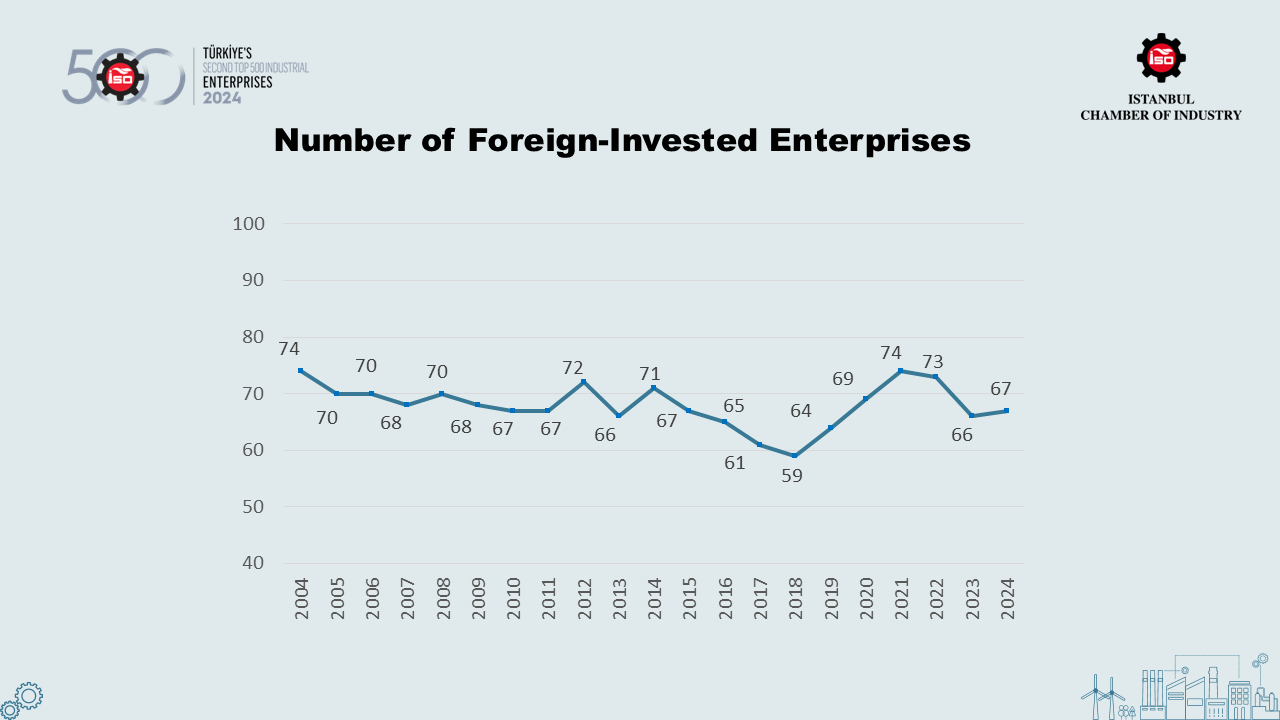

The number of foreign-invested companies in the ISO Second 500 increased between 2018 and 2021, followed by a pause in 2022 and then a sharp decline again in 2023. In 2024, the number of such companies rose by one to 67, maintaining a relatively stable trend.

Changes in the number of foreign-invested companies are influenced not only by shifts in firms’ capital structures but also by transitions between the ISO 500 and ISO Second 500 lists.

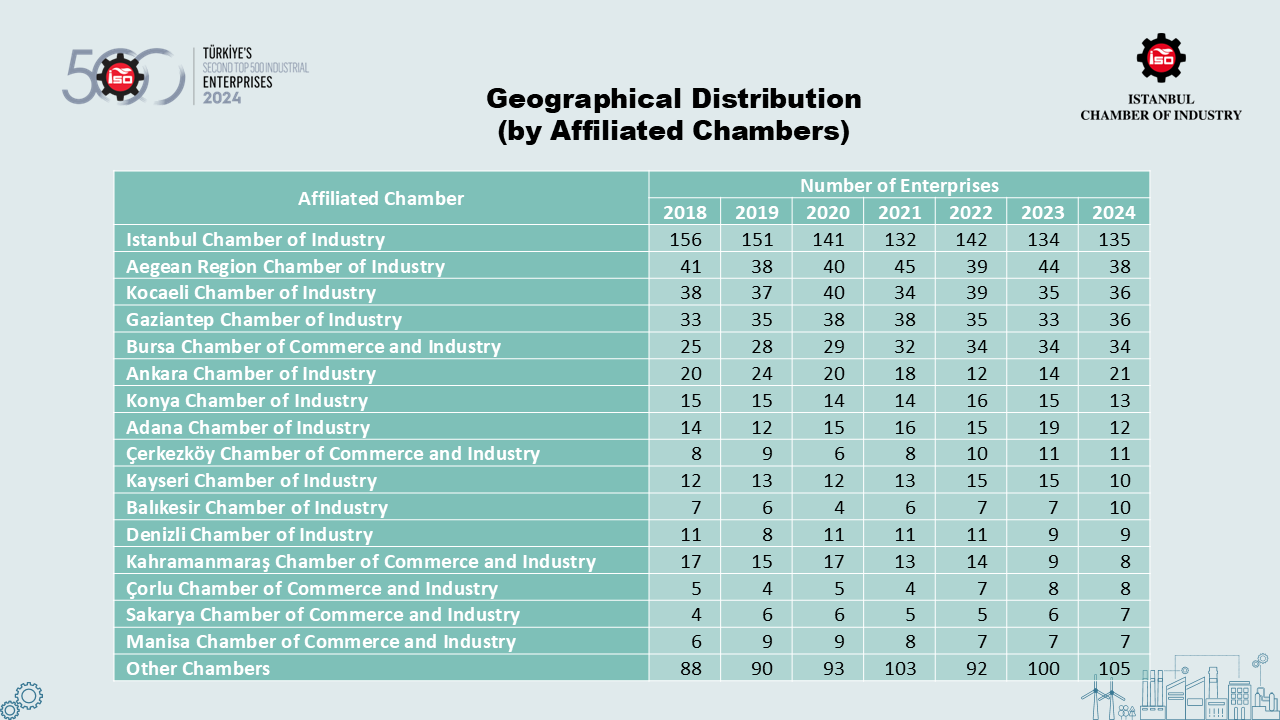

When the companies included in the ISO Second 500 are ranked according to their affiliated chambers, it is notable that the industrial presence in Anatolia has been increasing over the years and the distribution across Türkiye has begun to develop more evenly.

Despite a numerical decline in recent years, the Istanbul Chamber of Industry still holds the largest share within the ISO Second 500 with 135 companies. The number of member companies affiliated with the Istanbul Chamber of Industry increased by one in 2024. Following Istanbul, the Aegean Region Chamber of Industry ranks second with 38 companies, while Kocaeli and Gaziantep have 36, Bursa 34, and Ankara 21 companies, placing them among the top positions.

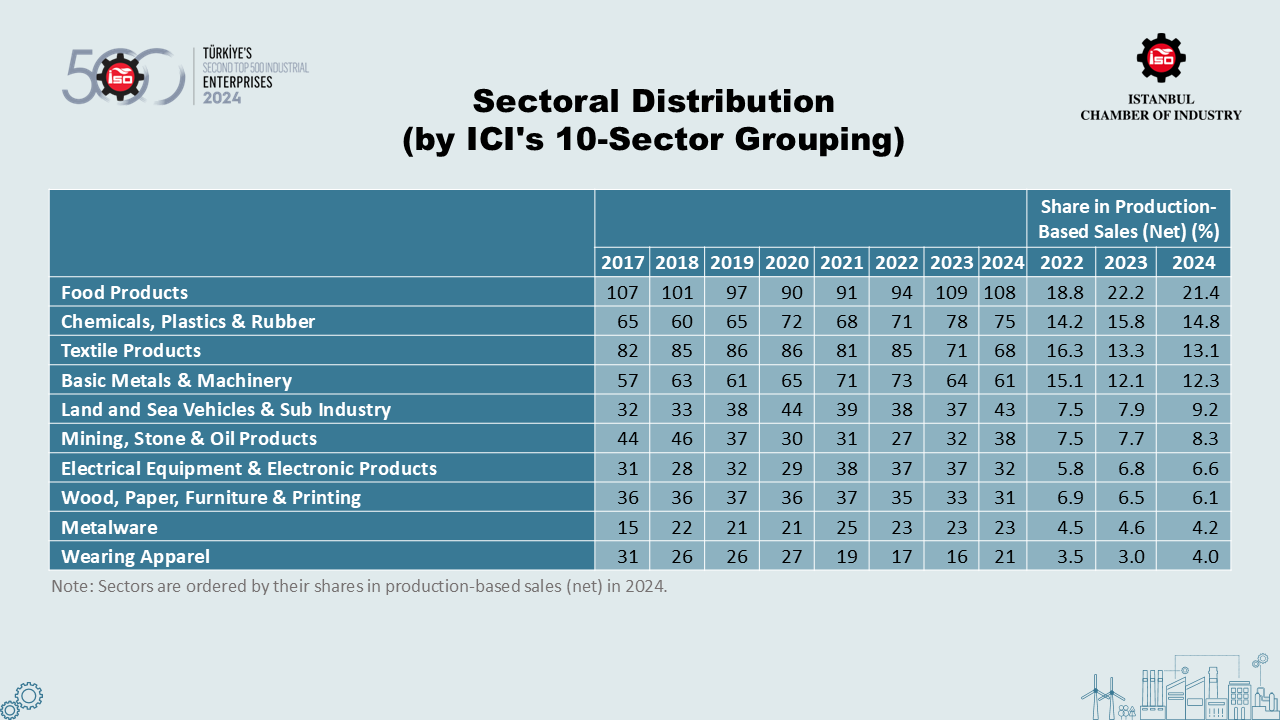

According to the distribution of the ISO Second 500 based on the 10-sector grouping created by the ICI, 62 percent of the companies are concentrated in four sector groups.

These are, respectively, the "food products" with 108 companies, the "chemicals, plastics & rubber" with 75 companies, the "textile products " with 68 companies, and the "basic metals & machinery" with 61 companies.

These four sectors also account for approximately 62 percent of production-based sales according to 2024 data. Meanwhile, the share of production-based sales for the top three sectors declined compared to the previous year, while the fourth sector showed a slight improvement in its share.

The ranking of the top 10 companies in 2024 ISO Second 500, based on net production-based sales, is presented in the table above. Accordingly, the company holding the first place in the ISO Second 500 was İstanbul Asfalt Fabrikaları San. ve Tic. A.Ş., with net production-based sales of TL 4.186 billion. This company ranked 283rd in the ISO Second 500 in 2023.

Following closely, Yılmaz Redüktör San. ve Tic. A.Ş. secured second place with net production-based sales of TL 4.185 billion. Yılmaz Redüktör was ranked 412th in the ISO 500 in 2023.

The third place went to Boyteks Tekstil San. ve Tic. A.Ş., with net production-based sales of TL 4.169 billion. This company was ranked 490th in the ISO 500 in 2023.

EN

EN